Monthly Markets Memo - April 2025

If we think of the first few months of 2025 as a classic storytelling structure, March very neatly fits the Rising Action portion of the plot. Aside from building tension, one of the other primary elements of the Rising Action phase of a plot is stakes increasing.

[Global Trade Tension Intensifies]

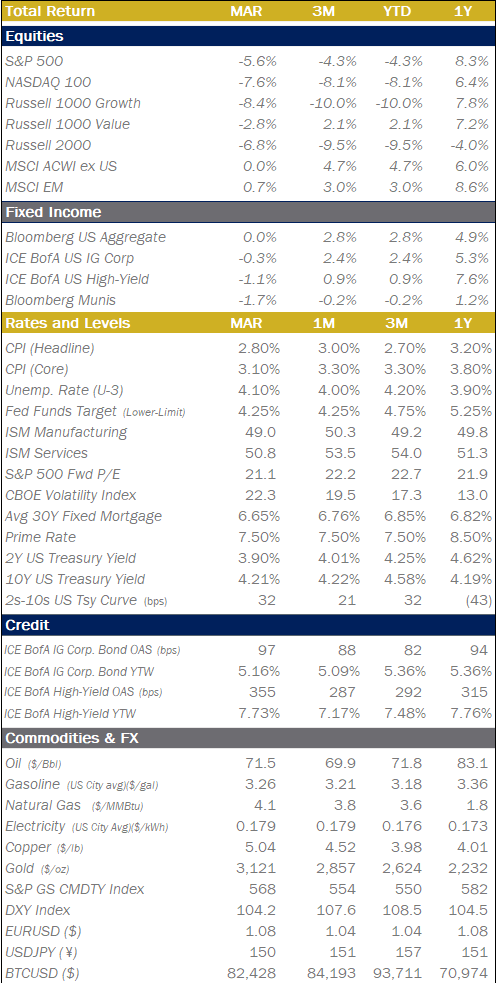

If we think of the first few months of 2025 as a classic storytelling structure, March very neatly fits the Rising Action portion of the plot. January and February were the Exposition, they set the stage, introduced the characters (new administration) and the central conflict (major policy changes, trade war with China). In March, the tension really starts to build as investors begin to rotate out of US equities in favor of Int’l Equities and Bonds. The S&P 500 briefly entered correction territory (-10%) in mid-March, before melting up into the end of the month. Meanwhile Q1 2025 was the first quarter in several years that US Large-Cap Stocks underperformed both International Stocks and US Bonds. Nearly all recent market trends reversed hard as investors began to reprice and retrench positions in the face of tariffs and the related economic fallout. Aside from building tension, one of the other primary elements of the Rising Action phase of a plot is Stakes Increasing. As stated in the last two market memos, independent of the ultimate level of new tariffs, the longer the uncertainty persists the more economic inertia dissipates. What initially started as a conversation about the possible inflationary effects of tariffs could result in more of a focus on the negative growth implications for the economy if the trade end-game remains elusive.

.png?lang=en-US "07-2024-Returns.png")

Quick Hits

Lowered Expectations

The University of Michigan’s Index of Consumer Expectations (distinct from its more famous sibling, the UofM Consumer Sentiment Index) hit its lowest level since July 2022. Further, while some surveys of consumers can be influenced by swings in politics, UofM in its report made clear that the decline in consumer expectations among respondents was observed across all demographic and partisanship categories, stating: “Republicans joined independents and Democrats in expressing worsening expectations since February for their personal finances, business conditions, unemployment, and inflation.” Also noting that “two-thirds of consumers expect unemployment to rise in the year ahead, the highest reading since 2009.”

Big Tech Takes Big Hit

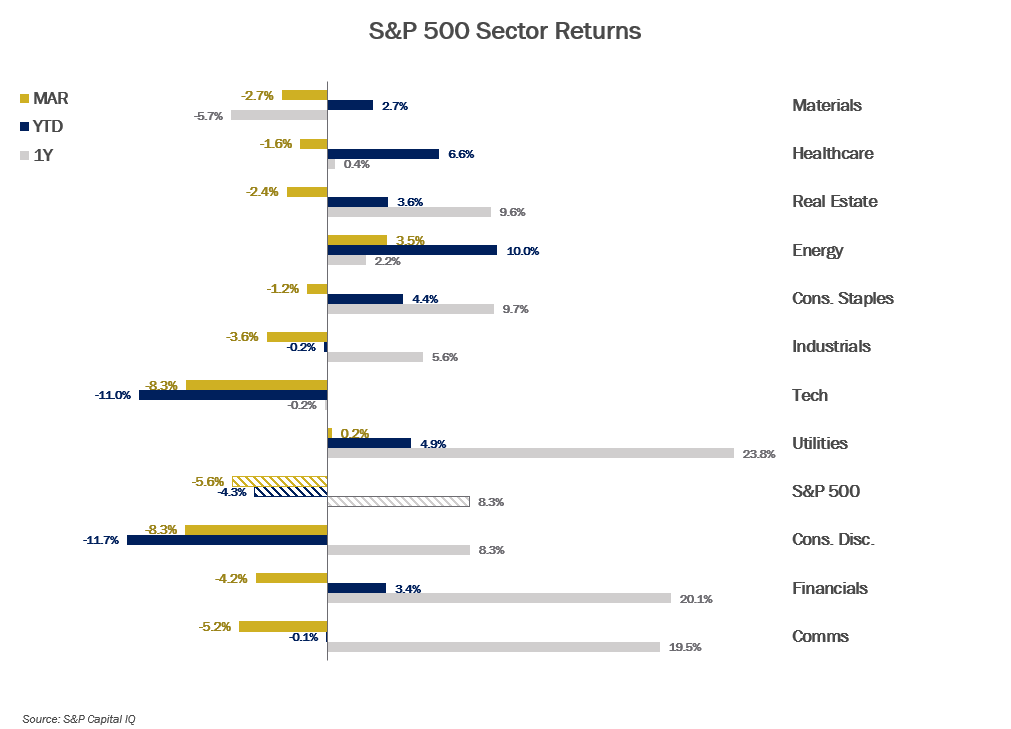

In 2023 and 2024, so-called “Magnificent 7” mega-cap technology stocks have been the main driver behind the overall S&P 500 index return. Q1 2025 was the first time since the inflation spike of 2022 that these Mag 7 stocks proved to be a bigger drain than boost on the index. The S&P 500 returned -4.6%, but if you excluded these 7 companies (that now constitute over 30% of the market cap-weighted index) from the returns, the other 493 companies combined for a positive 0.4% return in Q1.

FOMC Dot Plot Thickens

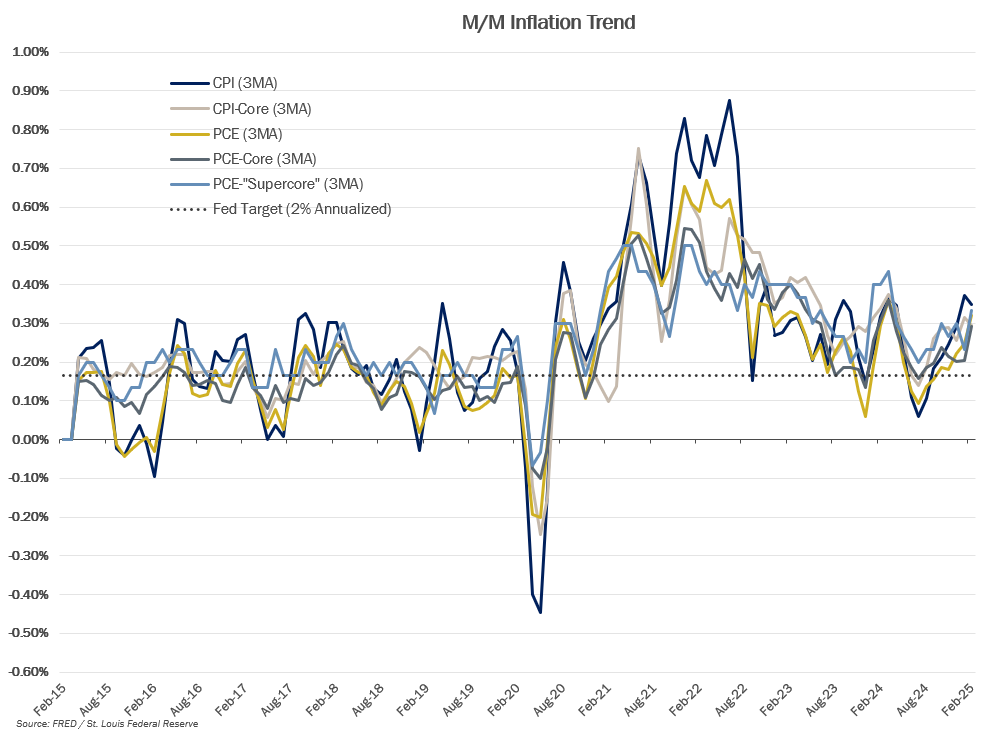

The FOMC kept rates on hold in their March meeting, but changes in the quarterly Summary of Economic Projections (SEP) reflected the growing angst on the committee regarding the expected economic effect of tariffs. While no change in the outlook for the Federal Funds rate was signaled, members increased their estimates of 2025 year-end inflation levels and decreased their estimates of 2025 and 2026 GDP growth rates. For those keeping score at home, that’s a stagflationary shift in outlook from the FOMC.

Number of the Month

The total decline in market value for Russell 1000 companies since the end of March, largely attributable to the announced tariffs.

.png")

On Deck this Month

- 04/01 – ISM Manufacturing (Mar), JOLTS (Feb)

- 04/02 – “Liberation Day”, President Trump Tariff Announcements

- 04/04 – ISM Services (Mar)

- 04/04 – Employment Report (Mar)

- 04/10 – Consumer Price Index (Mar), The Masters golf tournament begins

- 04/11 – Producer Price Index (Mar)

- 04/16 – Retail Sales (Mar)

- 04/18 – Good Friday Holiday (Banks and Markets closed)

- 04/20 – Easter Sunday

- 04/23 – Manufacturing and Services PMIs (Apr Flash reading)

- 04/28 – Amazon Q1 earnings, kicks off a week of Mag-7 earnings

- 04/29 – Consumer Confidence (Apr), JOLTS (Mar)

- 04/30 – Q1 Real GDP (1st Estimate), PCE (Mar), Employment Cost Index (Q1)

Chart of the Month: Anecdotes of Anxiety

Using word counts of the free-response commentary of Texas business executives given in the FRB-Dallas’ monthly Texas Service Sector Outlook Survey, it’s clear that “Uncertainty” about “Tariffs” is the primary issue on the minds of Texas-based business owners and executives. While “Uncertainty” certainly featured prominently in the October survey, that was in regards to the US election outcome. Given the volatile state of play around the announcement of tariffs, then incremental roll-backs. It wouldn’t be a surprise to see these topics continue to stay top-of mind for Texas-based business owners and executives for the foreseeable future.

Equities

.png")

.png?lang=en-US "MMM-Graph-3-Equities-2.png")

.png?lang=en-US "MMM-Graph-3-Equities-3.png")

Fixed Income

.png?lang=en-US "MMM-Graph-4-US-Treasury.png")

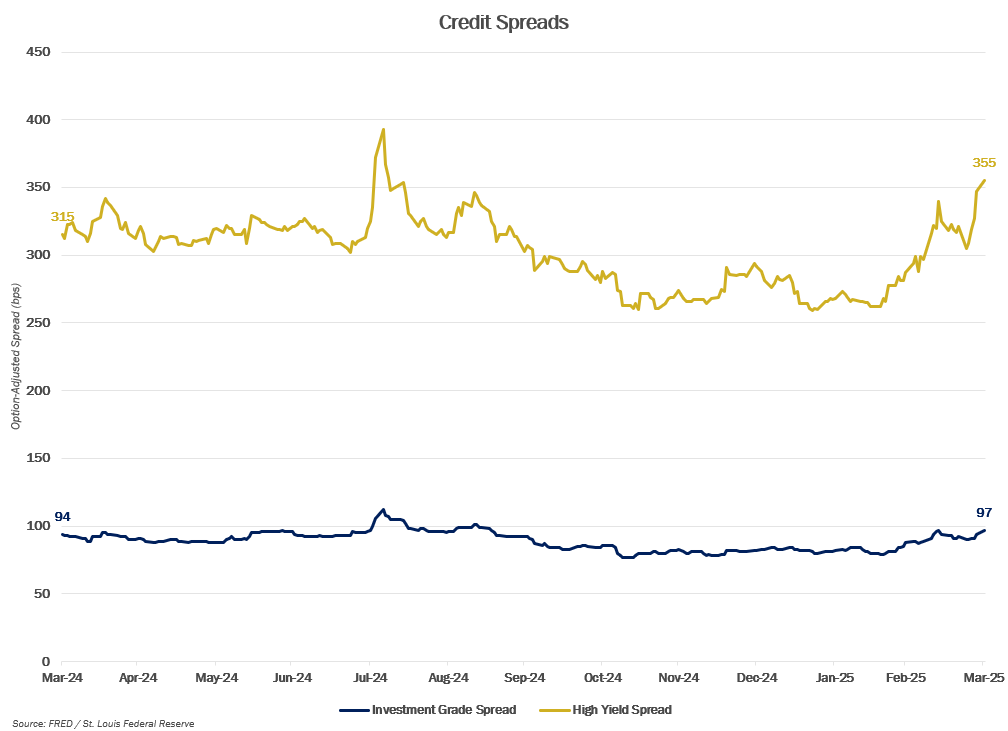

.png?lang=en-US "MMM-Graph-2-Credit-Spreads.png")

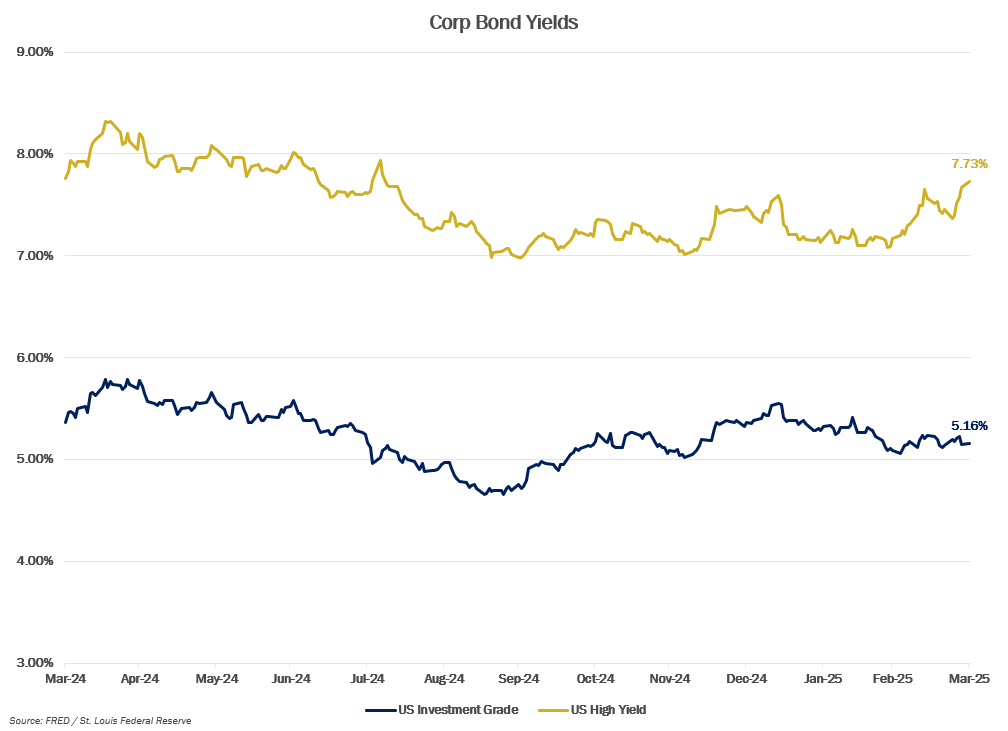

.png?lang=en-US "MMM-Graph-5-Crop-Bond.png")

Economic Data

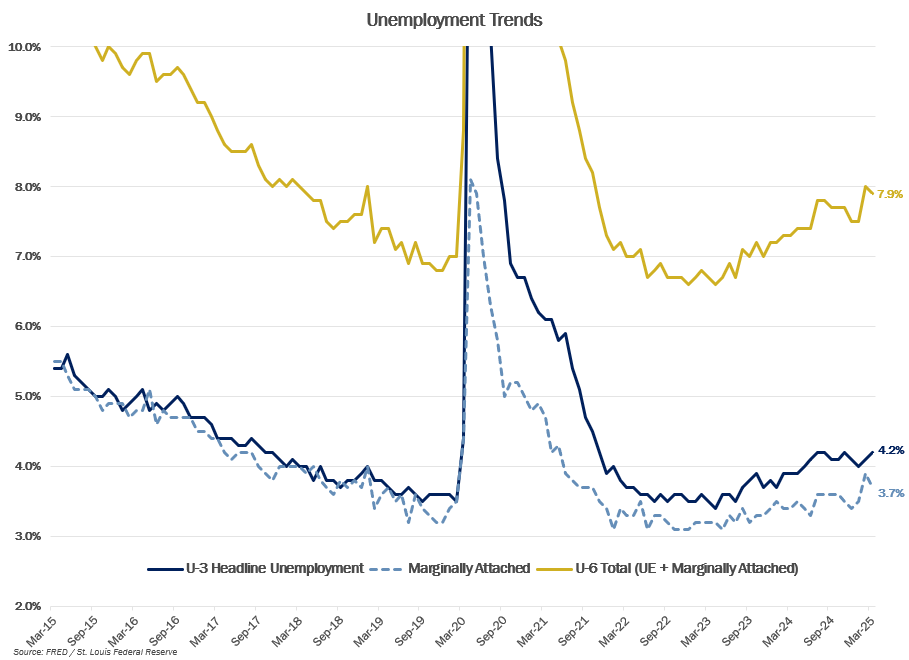

.png?lang=en-US "MMM-Graph-6-Unemployment-Trends.png")

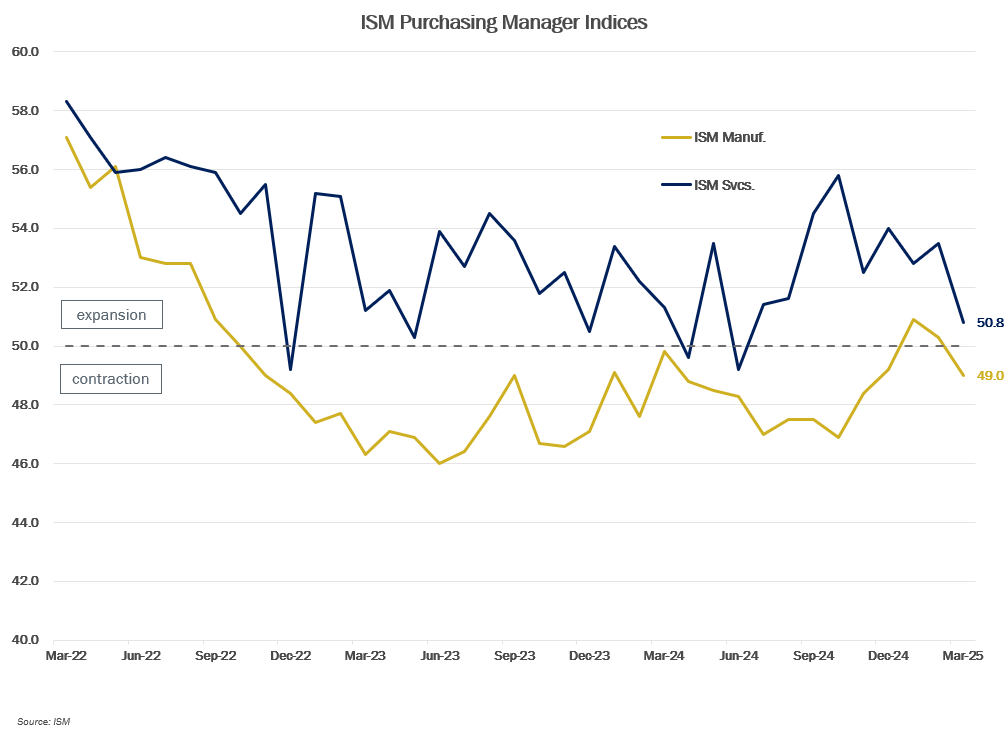

.png?lang=en-US "MMM-Graph-7-ISM.png")

.png?lang=en-US "ECON-Inflation-Trend-(1).png")

Serving Generations of Texas Families

We attain an in-depth understanding of our clients’ immediate and long-term goals, collaborating with their advisors to create a comprehensive financial plan, unique to them and their family.

INVESTMENT AND WEALTH SERVICES: Not a deposit | Not FDIC insured | No Bank guarantee | May lose value