Monthly Markets Memo - August 2024

July serves as a key reminder that adaptability and flexibility in the face of the unexpected are key to sustainable growth, whether it’s in our businesses, portfolios, or our communities. Keep your head on a swivel out there.

Hurricane Season

Given all the geopolitical and market events crammed into the back half of July, you could be forgiven for forgetting that a hurricane hit our state just a few days after the 4th of July holiday. Our friends in the Houston-area have not forgotten the many days without power and the literal tons of tree limbs that remain piled up around the city.

The path and development of Hurricane Beryl was a microcosm of a dynamic that we often see play out in markets, politics, and our daily lives. We observe a change in trend, construct a narrative around it, and then extrapolate this new trend into a set of expectations about the future. In the case of Hurricane Beryl, the usual tropical models were forecasting landfall in South TX or the Coastal Bend, but they failed to see the conditions that would steer the storm further North into Matagorda Bay and the Houston area. As a result, there was a rapid reset in expectations for the people and businesses of the Coastal Bend and Houston. As folks from Corpus Christi to Rockport finished boarding up windows for what ultimately amounted to an afternoon shower, everyone from Freeport to The Woodlands scrambled to stock up on supplies and prayed the power outages would be short. Even a professional, publicly traded utility was caught essentially flat-footed.

Similarly, market participants ended the month of June confident in the narrative that it’s not IF the Fed will achieve a soft-landing, but WHEN. Naturally, the month of July saw the release of data that indicated possible cracks in what was considered solid foundation: the employment market. First, the ISM Manufacturing and ISM Services Indices (reliable indicators for the direction of economic activity) for June reported below estimates, with both readings landing in contractionary territory, particularly amongst the hiring component of the index. The ISM Services Index reported the lowest level since May 2020. This disappointing economic data was quickly followed by the June Employment Report, showing a strong headline payroll number, but prior month revisions were significantly negative (-110k). Most concerning: the Unemployment Rate increased to 4.1% against expectations of remaining at 4.0%. Further surprising, yet welcome, economic data: CPI declined -0.1% in the month of June, and 3.0% Y/Y, reporting below expectations and a resumption of the disinflationary trend that had been interrupted this past Spring.

The clearest market reaction to this raft of economic data was a rapid reprice of the bond market accounting for the likely shift in the FOMC’s view of the balance of risks to its dual mandate: price stability and full employment. For nearly two years, the FOMC has had the luxury of focusing almost exclusively on stamping out inflation, but now the job market is looking less-than-perfect, and inflation looks to be making “further progress towards the Committee’s 2 perfect inflation objective.” To that end, we saw treasury yields decline through the month, with the 2-yr yield falling 50bps, as bond traders priced in additional cuts by the Fed, expected to begin this Fall.

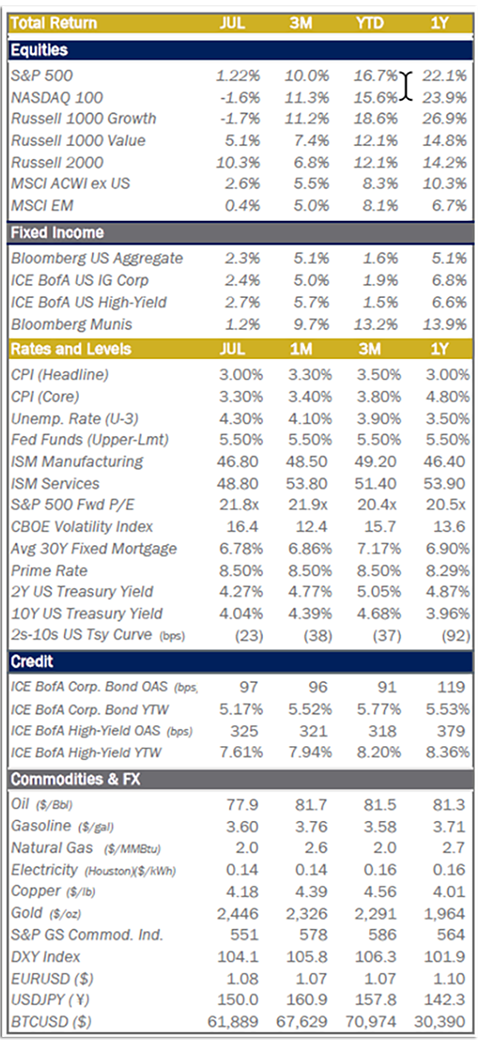

Meanwhile, in equities, the S&P 500 Index achieved a new all-time high on July 16th, propelled by positive news on retail sales and the lack of any negative consumer-related surprises in big bank earnings. Ultimately, equity indexes traded down through the back-half of the month as forward guidance from mega-cap technology companies disappointed investors and portfolios began to reposition for a new risk environment as the FOMC is expected to begin normalizing monetary policy.

July was a key reminder that adaptability and flexibility in the face of the unexpected are key to sustainable growth, whether it’s in our businesses, portfolios, or our communities. Keep your head on a swivel out there.

.png?lang=en-US "07-2024-Returns.png")

Number of the Month

The Sahm Rule, named for Fed Economist, Claudia Sahm is a recession indicator that flashed red when the 3-month average unemployment rate increases 0.50pp. When the indicator hits 0.5 or higher, that has historically indicated that the economy is already in the beginning stages of recession. If the July UE Rate comes in at 4.2%, the Sahm Rule will be triggered. That said, most typical indicators of recession: consumer spending, business investment, layoffs, etc are showing positive to benign levels. What is likely occurring is a very irregular shift in the labor force, driven by immigration and fading effects of the pandemic.

Quick Hits

Wildest July in US Presidential Election History

Potential disaster for US democracy was dodged as former President Trump survives an assassination attempt at a rally in Pennsylvania. President Biden, responding to sustained pressure from his party following poor debate performance in late June, announced he was withdrawing his candidacy, and endorsed the nomination of Vice President Kamala Harris. As of July month-end, polls and prediction markets were predicting a very tight race.

Elections Around the World

An alliance of left-wing parties in France kept the far-right out of power, the shaky alliances are likely to limit any legislative momentum. The Labour Party swept elections in the UK to seize the majority for the first time in over a decade, Kier Starmer succeeds Rishi Sunak as Prime Minister. Venezuela’s Maduro claims victory in presidential election, international observers, including Chile and the United States, dispute the validity of the official election results, citing inconsistency of the results with exit polls.

Small Caps, Big July

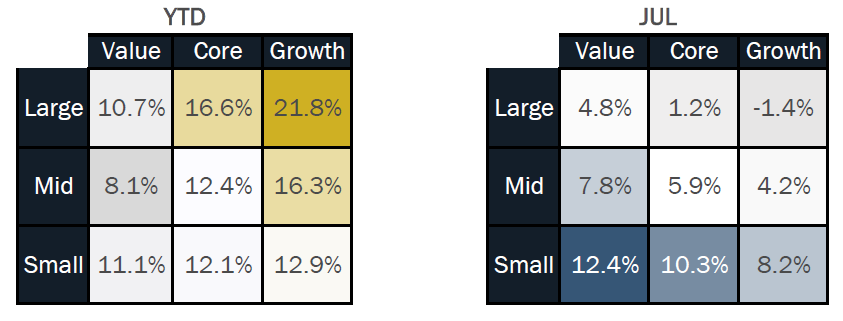

The small-cap benchmark Russell 2000 Index jumped an eye-popping 10.3%, closing the YTD performance gap to its large-cap peers. Small-caps benefited from a rotation trade out of richly-valued mega-cap tech stocks to interest-rate sensitive laggards like small-caps and REITs.

Sahm-Thing to Think About

Claudia Sahm’s (Former Fed economist) rule, an early-warning recession indicator, is likely to be triggered in the July or August employment report. It was developed in 2019 and shown to be 100% accurate in all US recessions going back to 1959. Stated simply, if the three-month average unemployment rate increases 0.5% relative to the lowest three-month average UE rate in the prior 12 months, then the indicator is triggered. The June employment report released in early July pushed the indicator to 0.43, the highest level since the COVID pandemic. It’s possible this time is different, as most economic data is not consistent with the view that the US is currently in recession, but the historical predictive power is something to ignore at your own risk.

On Deck this Month

- 08/01 – ISM Manuf. (July)

- 08/02 – Emp. Report (July)

- 08/05 – ISM Svcs. (July)

- 08/13 – PPI (July)

- 08/14 – CPI (July)

- 08/15 – Retail Sales (July)

- 08/21 – Minutes from Jul FOMC meeting

- 08/22 – Flash PMIs for August / KC Fed Jackson Hole symposium begins

- 08/29 – TX HS football season kicks-off / 2nd estimate of Q2 GDP

- 08/30 – PCE (July)

- 08/31 – Texas College football season kicks-off

Chart of the Month

The Bureau of Labor Statistics defines the 25-54yo age group as the Prime-age population. In recent months, the Prime-age labor force participation rate (LFP) has achieved levels not seen since before the dot-com bubble and China’s admission into the WTO. Labor Force Participation is defined as those currently employed or seeking work divided by the total population. One of the possibly benign (for now) reasons for the recent increase in the Unemployment Rate is that more people are entering the labor force and it’s taking longer for these new entrants to find employment, you can see this theory displayed by the rising gap between the Prime-age Employment-to-Population Ratio (EPOP) and the LFP. The level of those employed is steady in recent months, around 80%, while the LFP rate continues to rise. One can say it’s possibly benign for now, as it could be an influx of labor supply (e.g. migrant/immigrant workers). It could also be signs of a slow-down in labor demand that could ultimately transition from slow hiring to resulting in actual layoffs, and more serious increases in the unemployment rates.

Equities

.png?lang=en-US "MMM-Graph-3-Equities-(2).png")

Fixed Income

Economic Data

Serving Generations of Texas Families

We attain an in-depth understanding of our clients’ immediate and long-term goals, collaborating with their advisors to create a comprehensive financial plan, unique to them and their family.

INVESTMENT AND WEALTH SERVICES: Not a deposit | Not FDIC insured | No Bank guarantee | May lose value