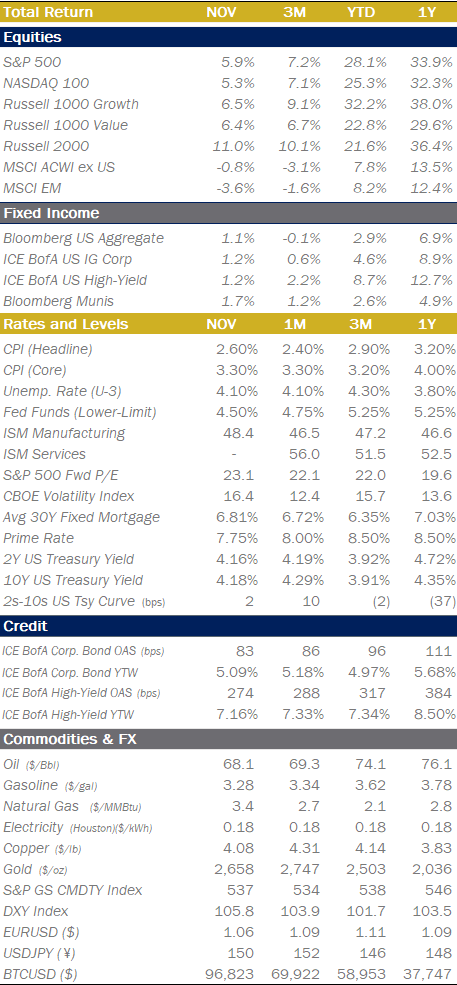

Monthly Markets Memo - December 2024

Contrary to expectations of a drawn-out election process, the outcome was clear by the end of election day, sparking a strong market reaction. With robust economic activity and stable inflation, the FOMC continued its rate cut path, setting the stage for further developments.

A November to Remember

The conventional wisdom held that election results would take days or weeks, with lawsuits, and judges possibly determining the outcome of a razor thin election; ultimately resulting in a likely split government. The conventional wisdom was wrong, again, and the election outcome was clearly trending to Trump before the end of election day in the Central time zone. The market reaction to this outcome was strong, with the US equities, represented by the S&P 500 index, ending the month higher 5.7%. While this move was surely driven in-part by resolution of a very big source of uncertainty, the level of “animal spirits” is palpable in markets as investors anticipate nearly full extensions of the TCJA tax-cuts, anticipated reduction in regulation, and a buoyant optimism amongst small business-owners and consumers that is showing up in various sentiment indices. Every investor’s biggest wish for the administration is being seen as likely and the bear-cases are being dismissed as mere heavy-handed campaign rhetoric. Markets’ confidence in the President-elect erring on the side of broad market preference seemed to be confirmed by some of the cabinet nominations that were ultimately announced after others were initially floated (e.g. Scott Bessent as Treasury Secretary).

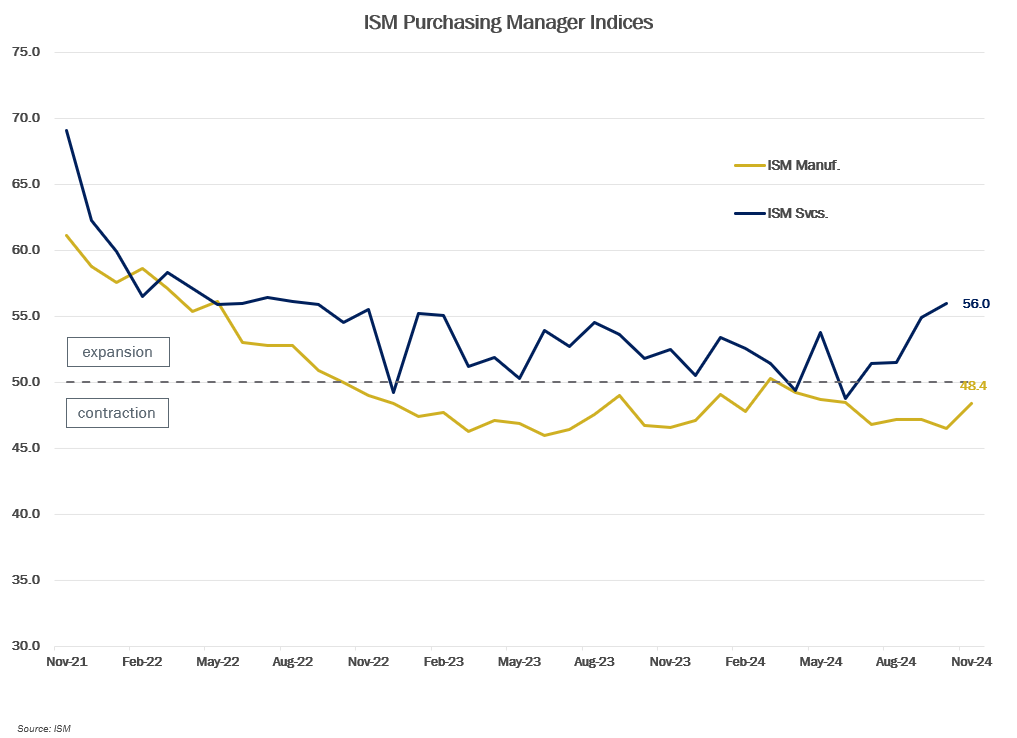

To further extend the theme of events flouting the narrative of conventional wisdom: the October jobs report came out on November 1, showing a mere 12,000 jobs added that month, missing expectations by nearly 100k. Markets shook this off entirely, there were no ructions in rates as markets frantically debated how the FOMC might react, they basically shrugged and chalked it up as noise from the economic impacts of hurricanes Helene and Milton. Speaking of economic impacts, the ISM Services index (a proxy for activity in the biggest portion of the US economy) increased in October and remains well-entrenched in expansion territory. The robust economic activity levels, coupled with inflation that remains stubbornly stable, gave the FOMC the data it needed to continue its rate cut path, lowering the Federal Funds Target level by 25bps to 4.50%-4.75% at the conclusion of its meeting on November 7.

.png?lang=en-US "07-2024-Returns.png")

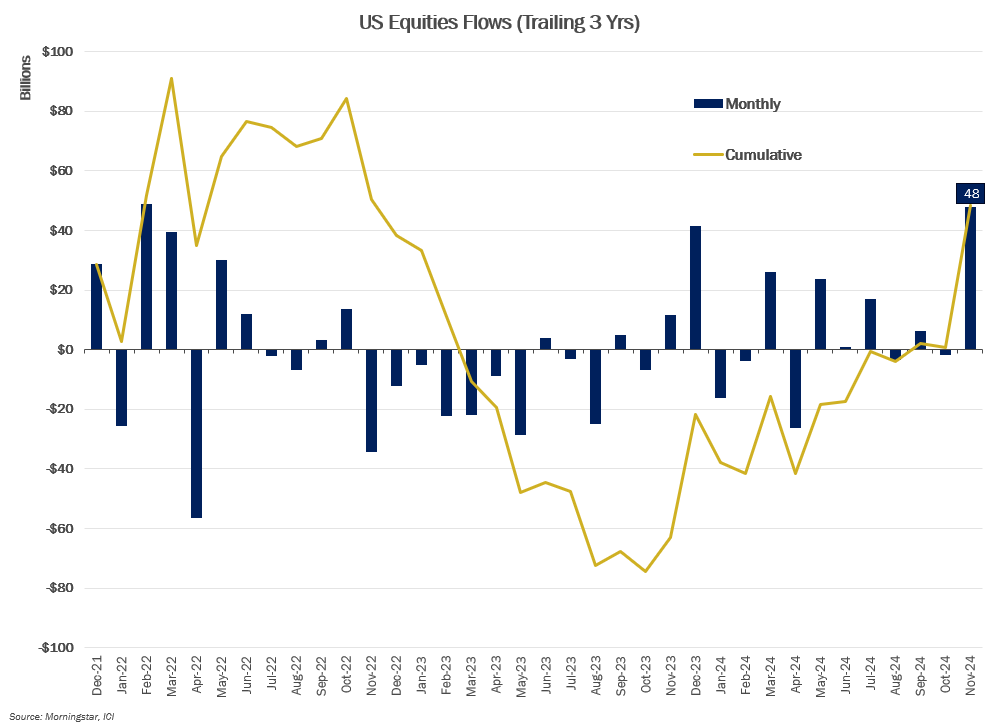

Number of the Month

The amount of money that flowed into US Equities funds in the month of November, following the outcome of US elections that resulted in the Republican party sweeping both houses of Congress and the White House. The largest monthly fund flow since February of 2022.

.png "Number-of-the-Month-(US-Fund-Flows).png")

Quick Hits

Care If I Tariff?

If there is one economic policy that is most closely associated with President-elect Trump, it’s his focus on trade and his preference for using Tariffs to achieve his policy aims. Markets are eagerly watching and weighing which threats of Tariffs are posturing for negotiations (e.g. the 25% tariffs on “all imports” from Canada and Mexico that he proposed on social media, which he backed off on once each country’s leader came to see him in person and made various commitments), and which he is likely to enact (e.g. an additional 10% tariff on all Chinese goods) and what the potential knock-on effects could be. Investors still recall December 2018 when an intensifying trade war with China introduced enough global economic uncertainty (coupled with a Fed hiking cycle and slowing growth) that stocks dropped 8-9% that month, erasing all gains for the entire calendar year.

Don’t Look Down

US Equities reached dizzying heights from both a pure price level and valuation standpoint. The S&P 500 Index level hit 6,000 for the first time ever, ending the month at 6,032.38. The Price to 12M Forward Earnings ratio (Fwd P/E) peaked at 23.1x on 11/29, a valuation level not seen since the frothy/frenzied time of Spring 2021.

On Deck this Month

- 12/02 – ISM Manufacturing (Nov)(Oct)

- 12/03 – JOLTS (Oct))

- 12/04 – ISM Services (Nov)

- 12/06 – Employment Report (Nov)

- 12/11 – CPI (Nov)

- 12/17 – Retail Sales (Nov)

- 12/18 – FOMC Meeting, Press Conf, & Projections

- 12/20 – PCE (Nov) & Consumer Sentiment (Dec)

- 12/18-12/21 Texas HS Football Playoff Finals (1A-6A)

- 12/25 – Christmas / Beginning of Hannukah (Markets Closed)

- 12/31 – New Year’s Eve (Final Trading Day of 2024)

Chart of the Month: “Trump Trade” Winners and Losers

“Elections have consequences” is often a trite phrase thrown around political talk shows, but for certain sectors of the economy this election result is proving very consequential.

The "Winners":

- Crypto assets. Coins, tokens and related equities (e.g. Coinbase) have shot up on the hopes that an SEC under a new administration might take a different view on crypto regulation (i.e. not treating crypto offerings like illegal/un-registered securities).

- Regional Banks. Various banking regulators under the Biden administration have made the approval process for potential bank M&A very opaque and uncertain, bank investors are anticipating that a new regulatory regime will unleash a wave of pent-up small and mid-size bank consolidation that will drive-up bank valuations.

The "Losers":

- Materials. Healthcare. China stocks: On the flip side, significant uncertainty around the scope, magnitude, and potential for trade-war dynamics has caused certain import-exposed sectors like Materials and Healthcare (i.e. Pharmaceuticals and Medical Supplies), as well as country-specific indexes (e.g. China) to lag broad market indices.

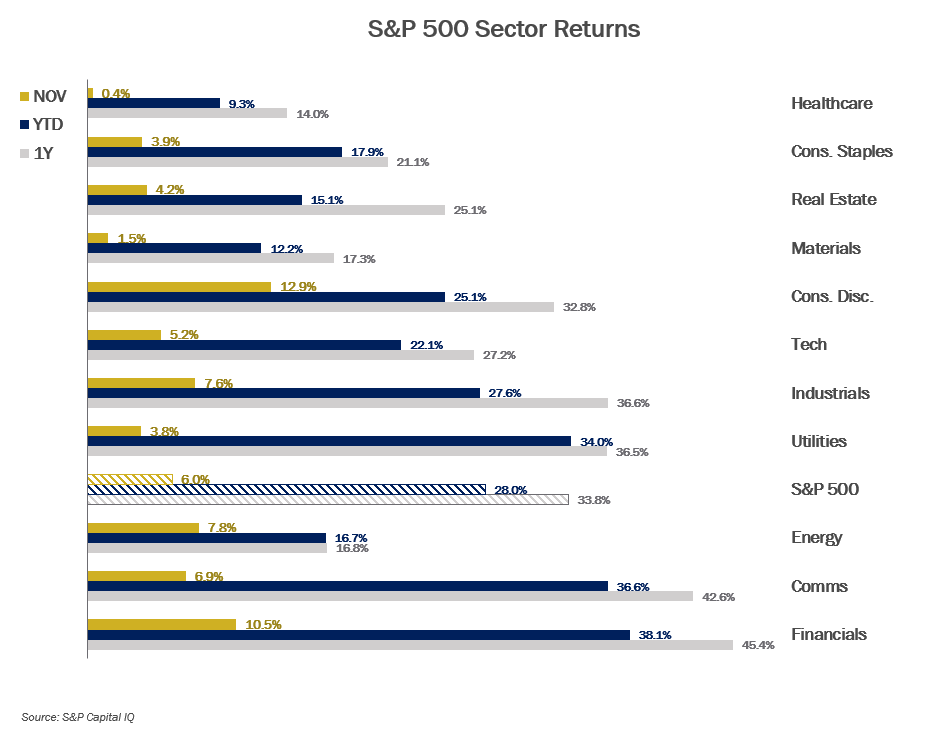

Equities

.png")

.png?lang=en-US "MMM-Graph-3-Equities-2.png")

Fixed Income

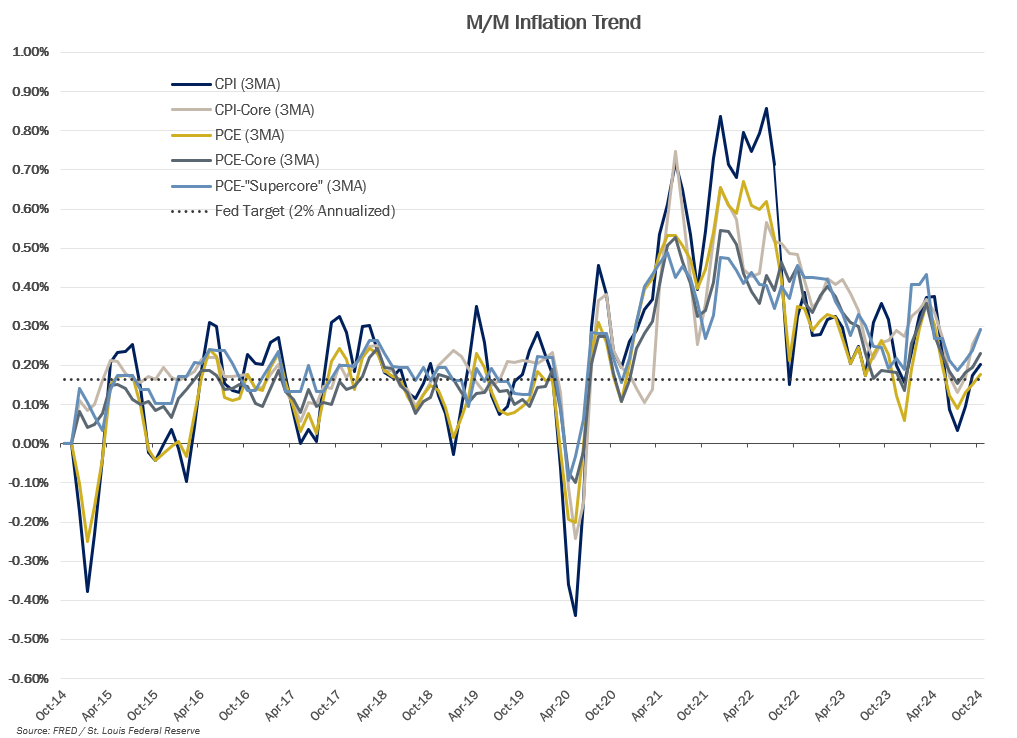

Economic Data

.png?lang=en-US "Econ-Inflation-Trend.png")

.png?lang=en-US "MMM-Graph-7-ISM.png")

Serving Generations of Texas Families

We attain an in-depth understanding of our clients’ immediate and long-term goals, collaborating with their advisors to create a comprehensive financial plan, unique to them and their family.

INVESTMENT AND WEALTH SERVICES: Not a deposit | Not FDIC insured | No Bank guarantee | May lose value