Monthly Markets Memo - February 2025

Policy uncertainty, unlike interest rate volatility, can't be hedged. This uncertainty aims to maximize negotiation leverage but challenges economic growth. As trade talks and legislative processes drag on, investors and business leaders may delay strategic initiatives, awaiting clarity on key policies.

The Uncertainty Principle

Nearly 100 years ago, in 1927, the German physicist Werner Heisenberg posited the uncertainty principle: in quantum systems there is a fundament limit to the precision with which certain pairs of physical properties can be observed simultaneously (e.g. the position of an electron, but not the linear momentum, and vice versa). While perhaps not a perfect corollary, the post-COVID macroeconomic environment has provided investors, corporate executives, and business owners a relative level of certainty and stability around fiscal and other governmental policies, with the primary source of anxiety being the outlook for interest rates. Beginning in late January 2025, what the market deemed known vs. uncertain shifted abruptly. The second Trump administration was inaugurated and wasted no time getting to work. While the general ethos of a more efficient government that is more aligned to conservative political principles was expected, the speed and breadth with which the executive branch of the government is being disrupted/reformed was not anticipated by much of the business and investor community. Further, and possibly most impactful: most observers anticipated tense trade negotiations and the imposition of additional tariffs between China and the US, likely followed by the US and EU with respect to specific industries (e.g. autos), and were caught off guard when the White House Press Secretary announced in a routine Friday afternoon briefing that 25% tariffs were to go into effect on all goods from Canada and the Mexico the following Monday. Ultimately, the tariffs were postponed an additional 30 days to allow for continued discussions between the close trade partners. This flurry of government policy activity, juxtaposed with a FOMC at a standstill as it observes stubbornly persistent inflation above its 2% target illustrates the handoff between sources of uncertainty.

Volatility of interest-rates can be managed with fixed-rate financing or interest-rate swaps, there is no financial instrument that can effectively hedge the risk of policy uncertainty (trade, tax, immigration, etc). The uncertainty and volatility is, in some sense, a desired outcome for the administration: it’s seeking to maximize leverage in negotiations with trade partners and to find fiscal room to maneuver a reconciliation bill through Congress. That said, as trade negotiations and the legislative sausage-making drags on, we are likely to see real headwinds to economic growth. Under such policy uncertainty, investors, corporate executives, and small business owners are likely to delay strategic growth initiatives as they await the new trade, tax, regulatory, and immigration (read: labor) inputs that are critical to their investment calculus.

.png?lang=en-US "07-2024-Returns.png")

On Deck this Month

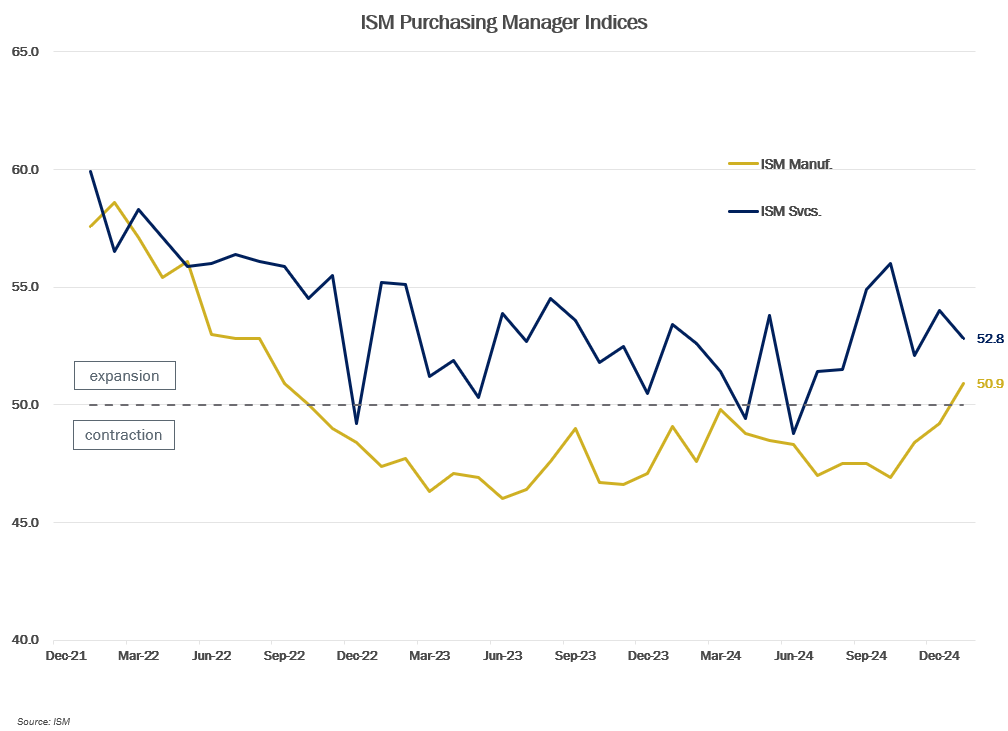

- 02/03 – ISM Manufacturing (Jan)

- 02/04 – JOLTS (Dec)

- 02/05 – ISM Services (Jan)

- 02/07 – Employment Report (Jan)

- 02/09 – Super Bowl LIX

- 02/12 – Consumer Price Index (Jan)

- 02/13 – Producer Price Index (Jan)

- 02/14 – Retail Sales (Jan)

- 02/17 – Presidents’ Day (Markets Closed)

- 02/21 – Existing Home Sales (Jan)

- 02/29 – FOMC Meeting

- 02/27 – 2nd Estimate Real GDP (Q4)

- 02/28 – PCE (Jan)

Quick Hits

Tariff Turbulence

The 25% tariffs threatened on all goods from Mexico and Canada came as a surprise, fortunately most of the time between the announcement and the eventual decision to postpone the implementation occurred during the weekend when markets were closed. For now, market participants appear to view the announcements and threats with skepticism, but that dynamic will likely have diminishing political returns for the administration. It’s possible that at some point they could actually be imposed. Academically, tariffs are inflationary on a one-time basis, but the pre-announced tit-for-tat reciprocal actions that are likely to be taken by various countries could have a longer last real-world inflationary effect, or at the very least, cloud the inflation data that the FOMC is using to make its rate decisions.

DeepSeek causes Deep Rethink

While most of the world was observing the inauguration of a new US President on January 20th, Chinese AI company DeepSeek released its r1 reasoning model. By that Sunday, the world had taken notice as DeepSeek’s related app had climbed to the top of the charts as the most downloaded apps on iOS and Android that week. With its release and related white paper, DeepSeek claimed to have achieved similar levels of benchmark output as OpenAI’s recently released reasoning model, but with a fraction of the time, computing power, and cost. Further, subject to US export controls, it should have had very little access to the NVDA chips considered to be the leading technology and crucial to any firm looking to scale their compute and train faster than others. In response, NVDA stock dropped 17% that following Monday. In the subsequent days and weeks, the market deduced that the original claim of achieving a high-level reasoning model on essentially $6M of spend was nuanced and not to be taken at face value, a permanent shift in the perception of what the winners and losers of the AI race might look like had taken shape. What I call “Leg 1” of the AI race, where the winners would be those that could raise and spend billions to buy the best GPUs (NVDA) to train their models the fastest and the only constraints were the supply of chips and the physical constraints on the pace of building datacenters is officially over. Inherent in the thinking of Leg 1 is that there is a clear “first-mover” advantage and that a lead can be insurmountable. What DeepSeek’s r1 shows is that ingenuity in seeking efficiency (some of the incumbents, like OpenAI, might rightfully call it “cheating”), such as training models on the output of other established models, can significantly cut into the lead of the large firms. While the incumbents like OpenAI will adjust how they allow and price the API calls on their current models to fend off these “efficiency hacks”, this new dynamic is likely to shape the next Leg of the AI race where efficiency and creativity are rewarded as handsomely as sheer scale.

Number of the Month

This is the US government “Debt Ceiling” that went back into effect on January 2, 2025 after its suspension in June of 2023. Markets and investors must once again contemplate the seemingly unthinkable as US legislators are expected to play another game of chicken with the world’s “risk-free” asset this summer.

Chart of the Month: Extraordinary Executive Orders

It’s not just you and your news feed, if it seems like President Trump has been signing a lot of executive orders the past few weeks, this chart quantifies exactly how many and shows that he has signed more that any other president in a single month since at least 1989. His signing hand must be cramping by now.

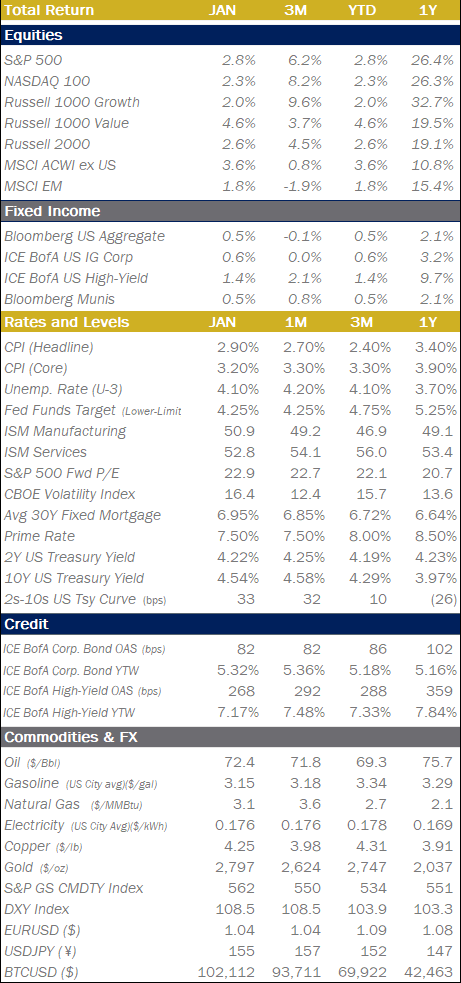

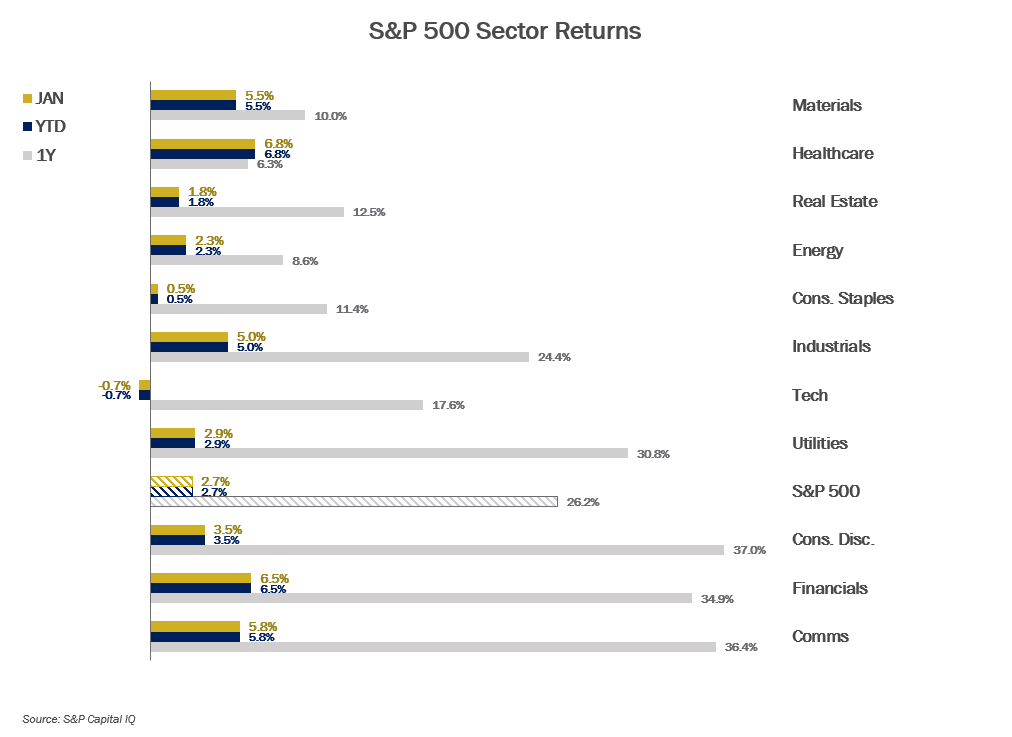

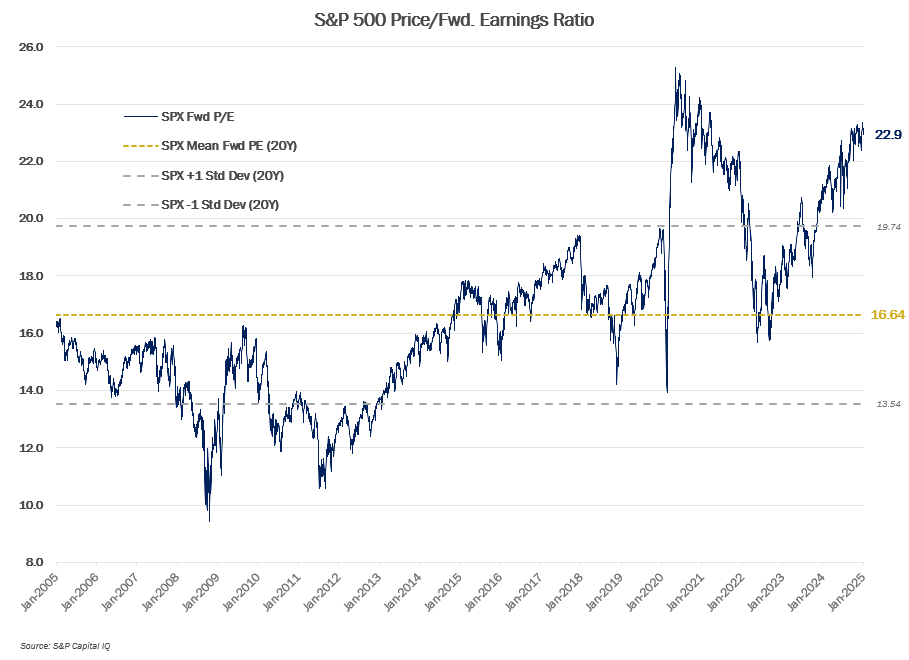

Equities

.png")

.png?lang=en-US "MMM-Graph-3-Equities-2.png")

.png?lang=en-US "MMM-Graph-3-Equities-3.png")

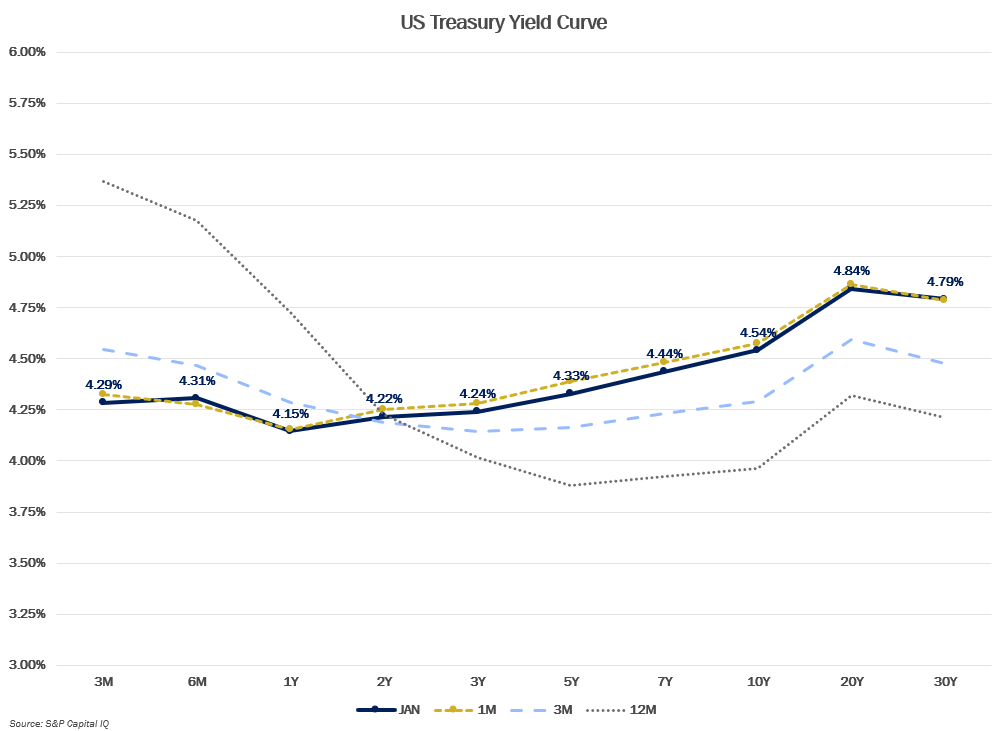

Fixed Income

.png?lang=en-US "MMM-Graph-4-US-Treasury.png")

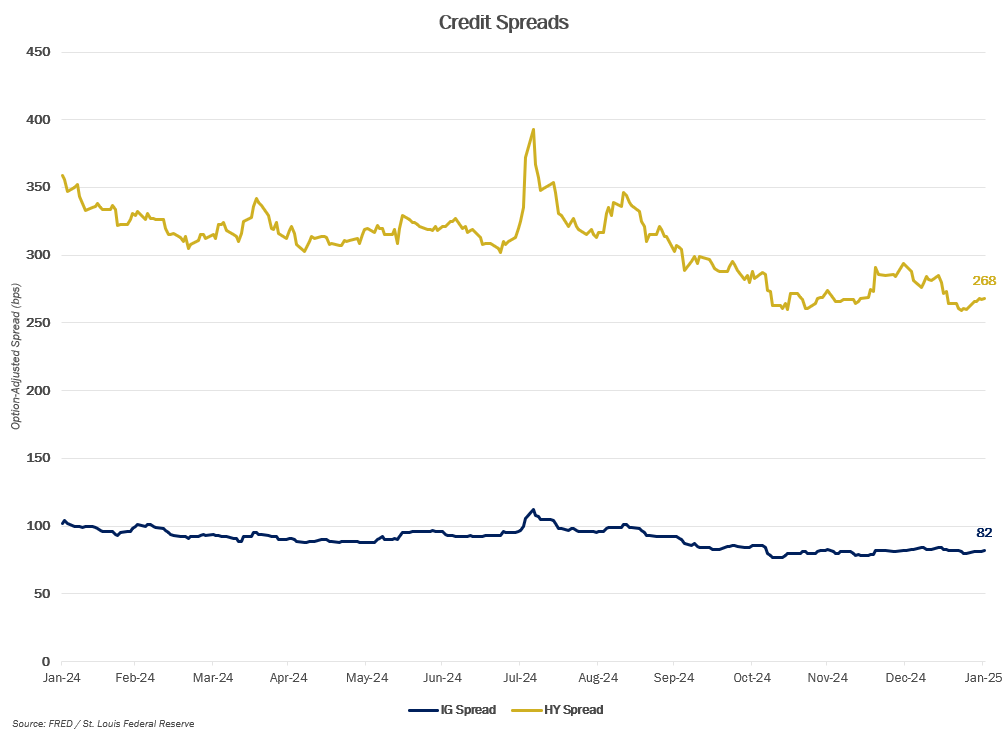

.png?lang=en-US "MMM-Graph-2-Credit-Spreads.png")

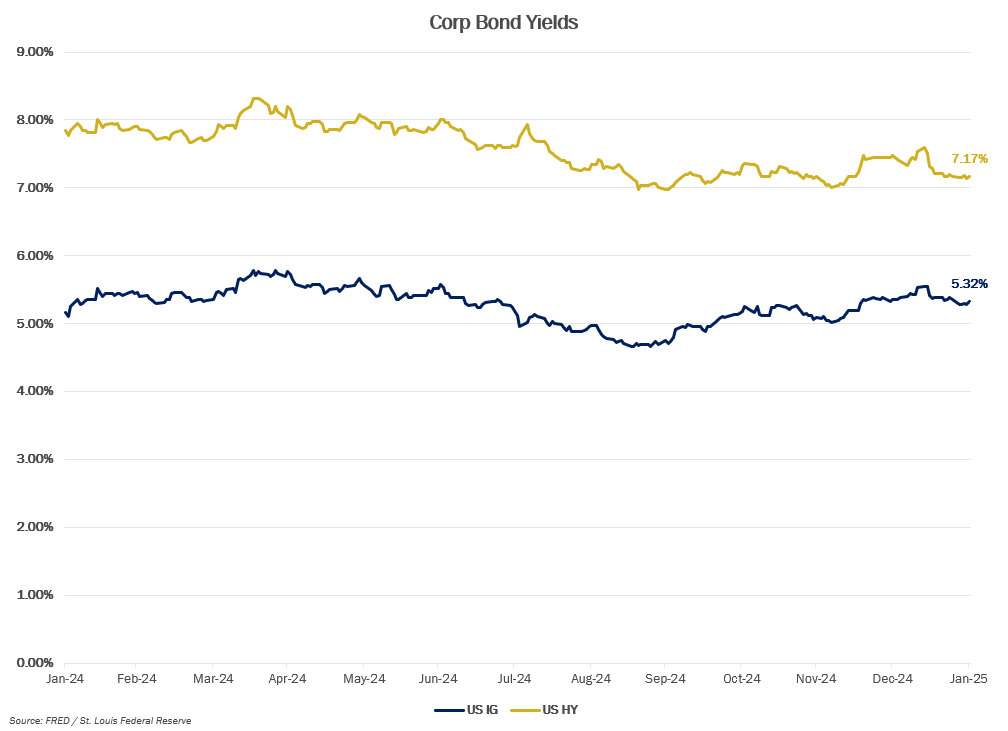

.png?lang=en-US "MMM-Graph-5-Crop-Bond.png")

Economic Data

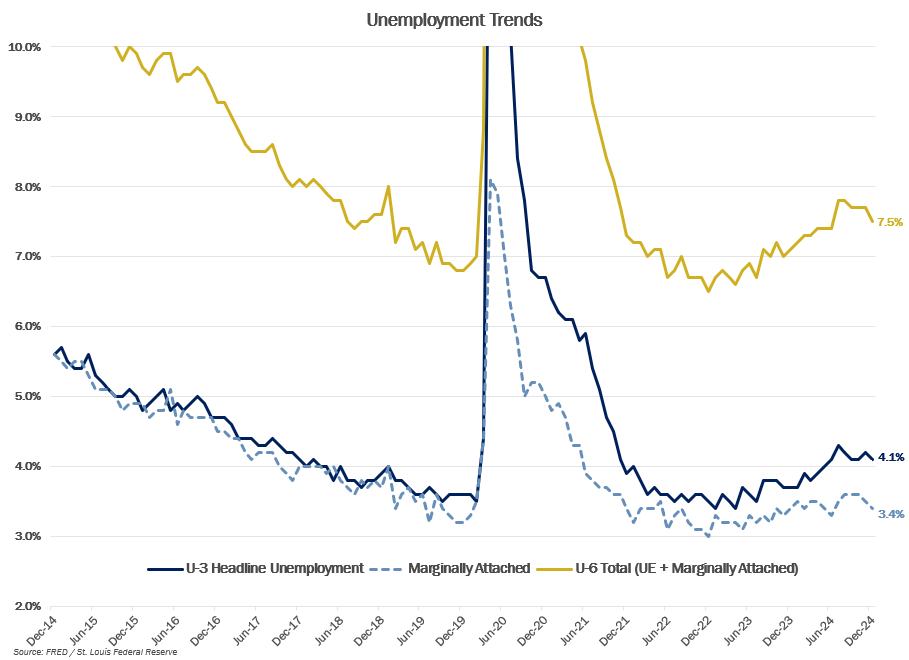

.png?lang=en-US "MMM-Graph-6-Unemployment-Trends.png")

.png?lang=en-US "MMM-Graph-7-ISM.png")

Serving Generations of Texas Families

We attain an in-depth understanding of our clients’ immediate and long-term goals, collaborating with their advisors to create a comprehensive financial plan, unique to them and their family.

INVESTMENT AND WEALTH SERVICES: Not a deposit | Not FDIC insured | No Bank guarantee | May lose value