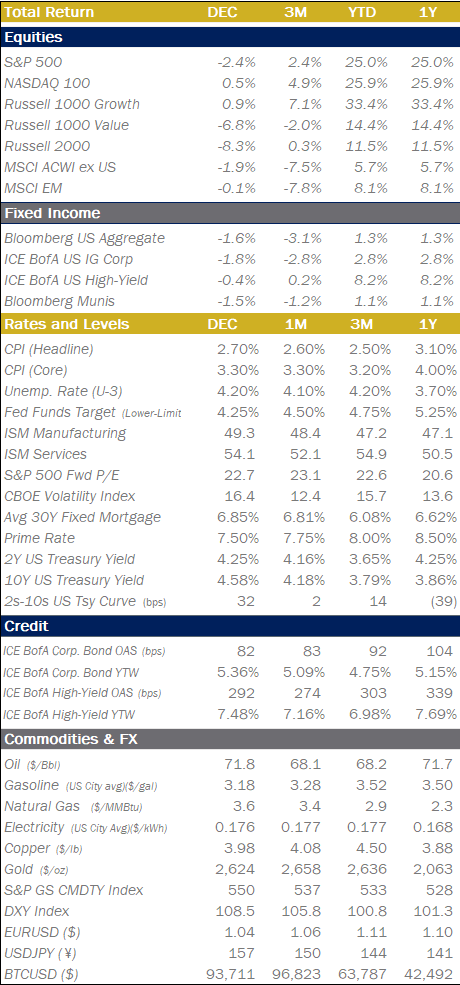

Monthly Markets Memo - January 2025

With markets showing no signs of worry and optimism fully priced in, expectations are high. The labor market is stable but slow, possibly signaling a shift from tight to softer conditions. While everything seems great now, the best time to prepare for winter is while the sun still shines.

Everything is Awesome vs. Is Winter Coming?

The human brain is an amazing organ that we still don’t have perfect insight and transparency into. The largest companies in the world are currently spending many billions of dollars per year to replicate the power of the brain, using vast amalgamations of silicon, copper, palladium and other elements, as opposed to neurons and gray matter. Among the multitude of mysteries the human brain contains, the ability to hold two seemingly oppositional thoughts at once is one of its unique capabilities.

The S&P 500 returned 25% in 2024, the unemployment rate is at 4.2%, consumer balance sheets haven’t been this strong in decades, and US real GDP continues growing at +3% rates, well above pre-pandemic trends. All of this macro-economic data and the exuberance of markets and business leaders regarding the prospect for tax-cut extensions and lower regulatory burdens with a new administration and congressional mix has most investors and consumers humming “Everything Is Awesome” (The Lego Movie, 2014) to themselves as we transition into 2025.

Everything is, indeed, pretty pretty good, and valuations across markets appear to fully reflect this; Fwd. P/E Ratios on the S&P 500 trade at two standard deviations above the 20-yr mean, and credit spreads are hovering above 20-yr tights. However, December’s chill came late as investors weighed a surprisingly hawkish outlook in the FOMC’s Summary of Economic Projections (SEP), showing fewer cuts in 2025 than the committee members had anticipated just three months prior in the September SEP, as well as a 2025 year-end inflation level that was also higher than the level anticipated in the September SEP. Markets reacted violently, with the 2nd largest spike in the VIX for all of 2024. Hopes for a Santa Claus rally were dashed, and coal was deposited in investors' stockings with US stocks, Int’l Stocks, and bonds all declining for the month of December.

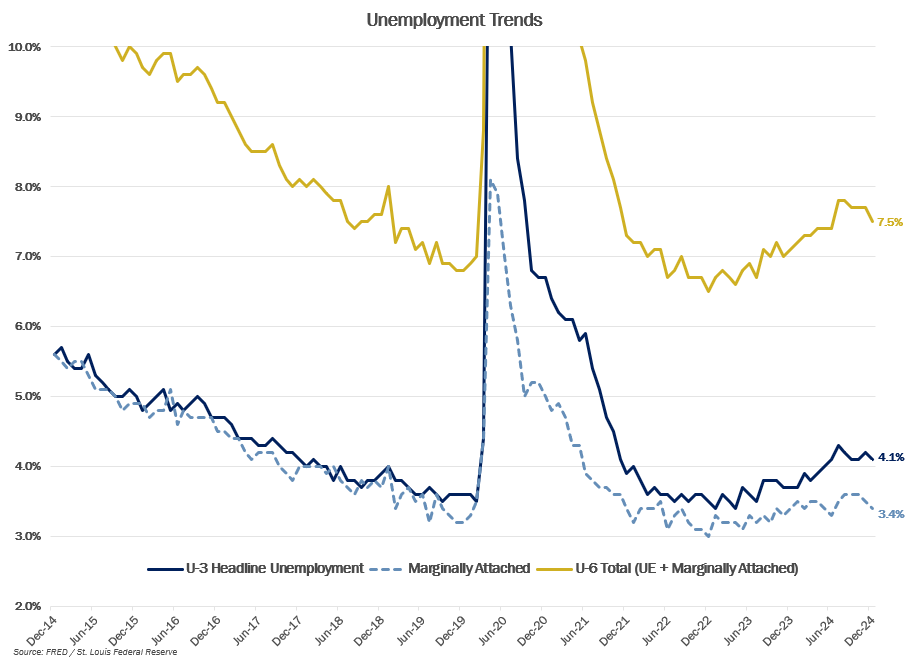

What leaves us wondering about the winds of winter, and whether it may truly be coming for asset prices, is the lack of a general wall of worry for markets to climb. When all the current news is good, and optimism for future changes are fully priced, there’s nothing left to temper expectations. With no hurdles to clear, the only upside catalysts higher will be stronger than expected earnings. As of today, the labor market is stable, and there’s no sign of increasing layoffs... but there is a notable slowness. It is taking longer for employers to hire and for job seekers to find employment. This disconnect between employers and job seekers could be a temporary issue as the labor market settles into a new equilibrium relative to the frenzy that occurred in the pandemic recovery. Or it could be the initial signs of the pendulum completing its swing from an extremely tight labor market to one that is too soft to sustain the low unemployment and strong consumption we have benefited from for nearly half a decade now.

To be sure, everything is awesome, but the best time to prepare for winter is while the sun still shines and the harvest is plentiful.

.png?lang=en-US "07-2024-Returns.png")

Number of the Month

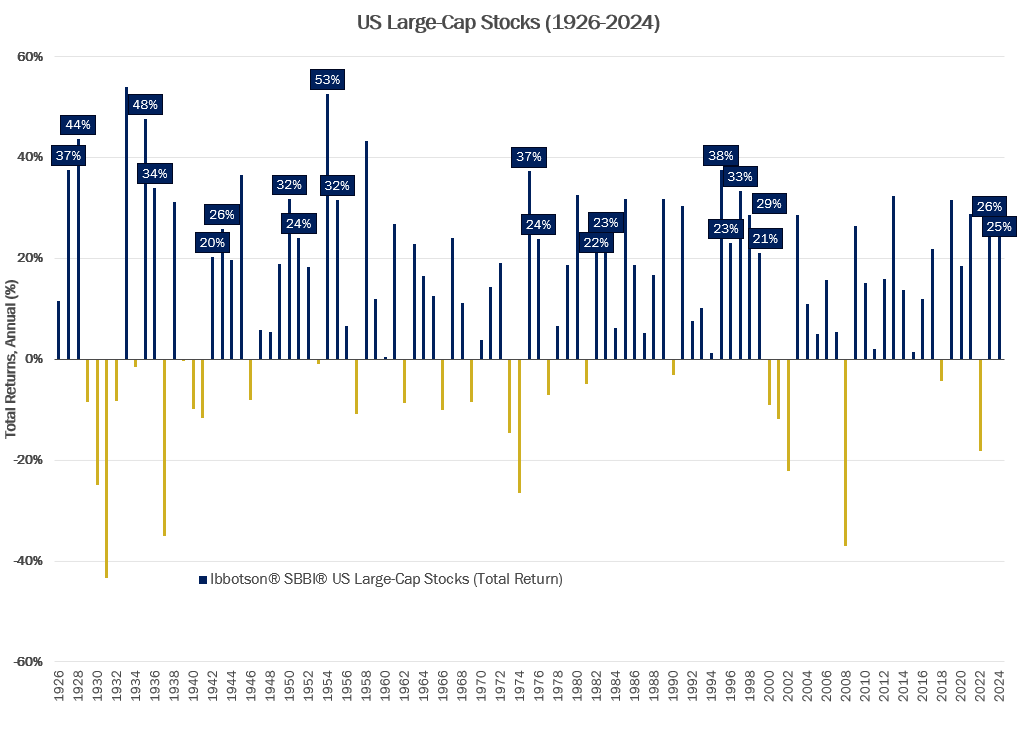

TWELVE. 12 times since 1926 have US Large Cap Stocks returned +20% in back-to-back years. While the relative rarity of this occurrence may give investors pause for stock returns in 2025, most (7 of 11) of those back-to-back periods have seen the third year result in positive stock returns also!

.png?lang=en-US "Number-of-the-Month-(US-Fund-Flows).png")

Quick Hits

The Waiting Place

In the October JOLTS report (released in December), the job market looks a bit like the "waiting place" from Dr. Seuss's "Oh, the Places You'll Go!" Job Openings crept up to 7.7M, above expectations, and Hires declined. It was another month where employers and job seekers seemed to be in a holding pattern, “waiting for a train to go or a bus to come, or a plane to go or the mail to come.”

China Econ Outlook Stays Dim Sum

When China announced measures to support financial markets and to stimulate the economy back in September, they were received as somewhat underwhelming by markets and there was an expectation that more would be announced. To date, there haven’t been any new measures, leading broad China equity indices to give back the majority of the gains they experienced in the initial response to the stimulus announcements. Chinese growth is set to be its lowest in years, and inflation is likely turning into deflation. 10Y Chinese Govt Bonds yields have rapidly declined to their lowest levels since 2000 and are trading below 2.00% yields. China faces a significant balance sheet recession as the real estate bubble pops and unwinds through every aspect of their economy. There are likely no simple or easy solutions, and anything that may speed the process will require scope and magnitude proportional to the size of China’s economy and its importance to global GDP. Meanwhile, all of this is occurring as a mere backdrop to what is also expected to be a complex/combative interaction with the incoming US administration regarding trade tariffs and continued technology supply chain competition.

Q4 Earnings and 2025 Expectations

As indicated in the opening parts of the memo, all the fun stuff like tax cut extensions and lower regulatory burdens are already priced into equities. The primary lever to drive equities higher is delivering and, ideally, exceeding expectations for earnings. Q4 earnings season kicks off on Wednesday, Jan. 15, with the biggest banks and financials. If earnings come in at current consensus estimates, that will represent 8% annual growth in S&P 500 earnings for 2024. That 8% profit growth for the broad index is largely driven by the massive profit growth at the mega cap tech companies that are broadly benefiting from the demand for their products and services in the AI gold-rush. The so-called Magnificent 7 as a group, are expected to report 33% earnings growth for FY 2024, while the remaining 493 companies together will report 3% growth in earnings. Markets are currently pricing 2025 EPS growth estimates that reflect a modest reversion in those growth rates between the Top 7 (18%) and the rest of the index (11%). This implies a broadening of the profitability growth to the rest of the index. Investors will be keenly focused on the forward guidance provided by the other 493 companies in the Q4 earnings calls over the next two months for indications of whether or not this is actually occurring. If and to what extent we do see this expected broadening will likely be the main source of volatility at the index level and within the index itself in the coming months.

On Deck this Month

- 01/01 – New Year’s Day (Holiday)

- 01/03 – ISM Manufacturing (Dec) (Oct)

- 01/07 – JOLTS (Nov)

- ISM Services (Dec)

- 01/09 – National Day of Mourning for Fmr. President Carter (Market closures)

- 01/10 – Employment Report (Dec)

- 01/14 – 89th Texas Legislature convenes

- 01/15 – CPI (Dec)

- Q4 Earnings Season kicks-off with major banks reporting

- 01/16 – Retail Sales (Dec)

- 01/20 – Martin Luther King, Jr Day (Markets & Banks closed)

- Inauguration Day for 47th POTUS: Donald J. Trump

- College Football Playoff National Championship Game

- 01/29 – FOMC Meeting

- 01/30 – 1st Estimate Real GDP (Q4)

- 01/31 – PCE (Dec)

- Employment Cost Index (Q4)

Chart of the Month: Long Treasury Yields Rising, Correlations Falling

For much of the last several years, the shifts up and down along the yield curve can be directly and nearly fully attributable to changes in the path of rate hikes or cuts from the FOMC. But in mid-November, the longer end of the yield curve is beginning to decouple from FOMC expectations. If we view the 2Y US Treasury yield as a proxy for FOMC sensitivity, as it is the yield that’s been and remains the most sensitive to potential changes in the Federal Funds target-range, we can measure the correlation of its movements with other tenors on the yield curve. As is illustrated in the chart, the 10Y is beginning to move in much less correlated ways from the 2Y, implying that the markets are trading the 10Y Treasury bond with a focus on something beyond just the FOMC reaction function. Potential explanations for this new development range from bond investors “finally” demanding some term premium (extra yield for locking up their cash for longer terms) to markets requiring higher yields to account for increasing anxiety and risk around the fiscal situation and where it may be in a decade. As is often the case with markets, the real explanation is probably a weighted average of all the possible explanations. But one thing is for certain: something has materially changed in the bond/rates market; ignore it at your own peril.

Equities

.png")

.png?lang=en-US "MMM-Graph-3-Equities-2.png")

Fixed Income

Economic Data

.png?lang=en-US "MMM-Graph-6-Unemployment-Trends.png")

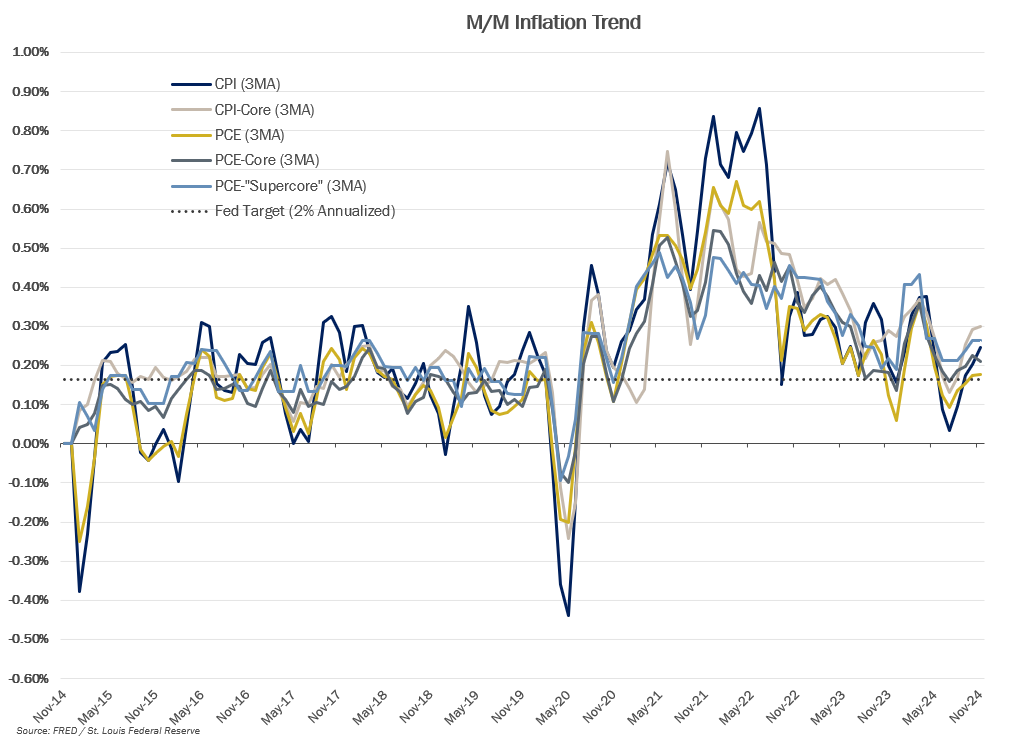

.png?lang=en-US "Econ-Inflation-Trend.png")

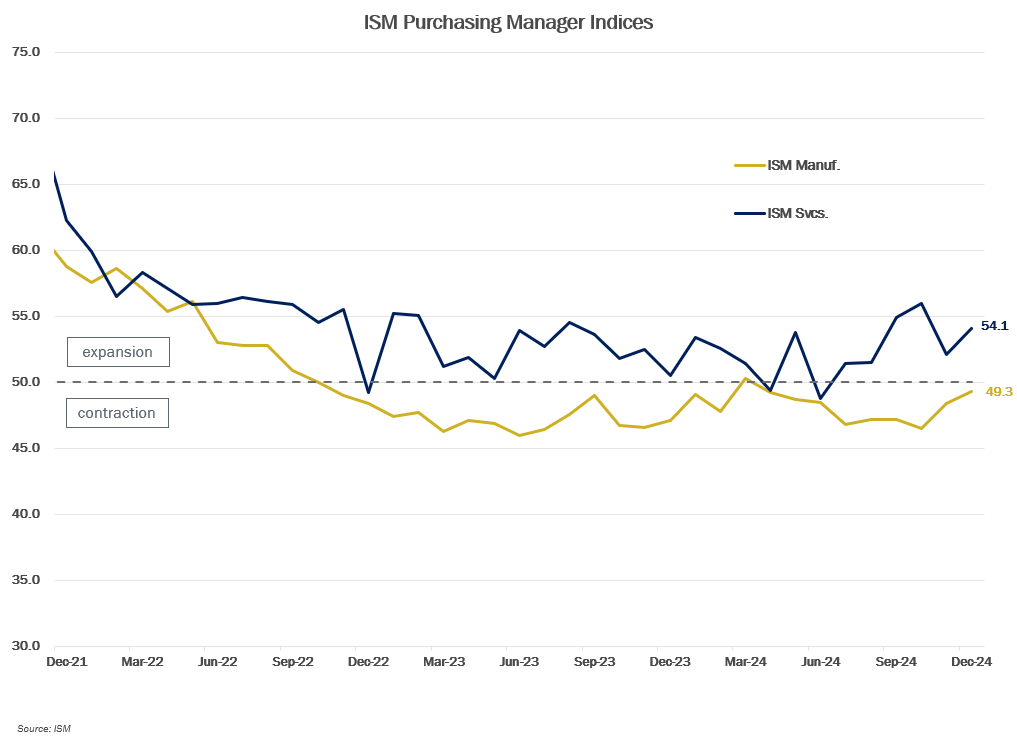

.png?lang=en-US "MMM-Graph-7-ISM.png")

Serving Generations of Texas Families

We attain an in-depth understanding of our clients’ immediate and long-term goals, collaborating with their advisors to create a comprehensive financial plan, unique to them and their family.

INVESTMENT AND WEALTH SERVICES: Not a deposit | Not FDIC insured | No Bank guarantee | May lose value