Monthly Markets Memo - July 2025

Markets roared into the second half of 2025 with broad-based strength, shrugging off geopolitical shocks as investor optimism surged. But beneath the rally, a high-stakes game of chicken is brewing between markets and the White House over trade policy.

We’re So Back (..but so are Tariffs)

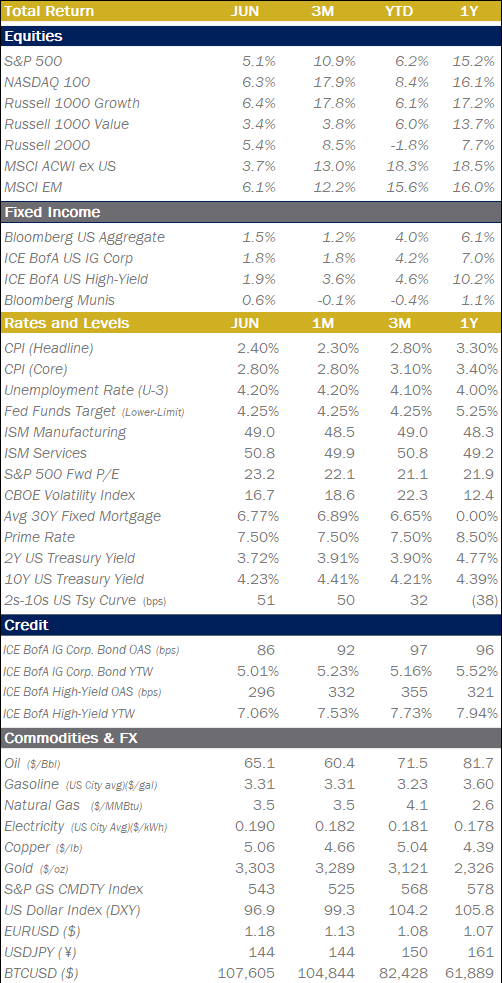

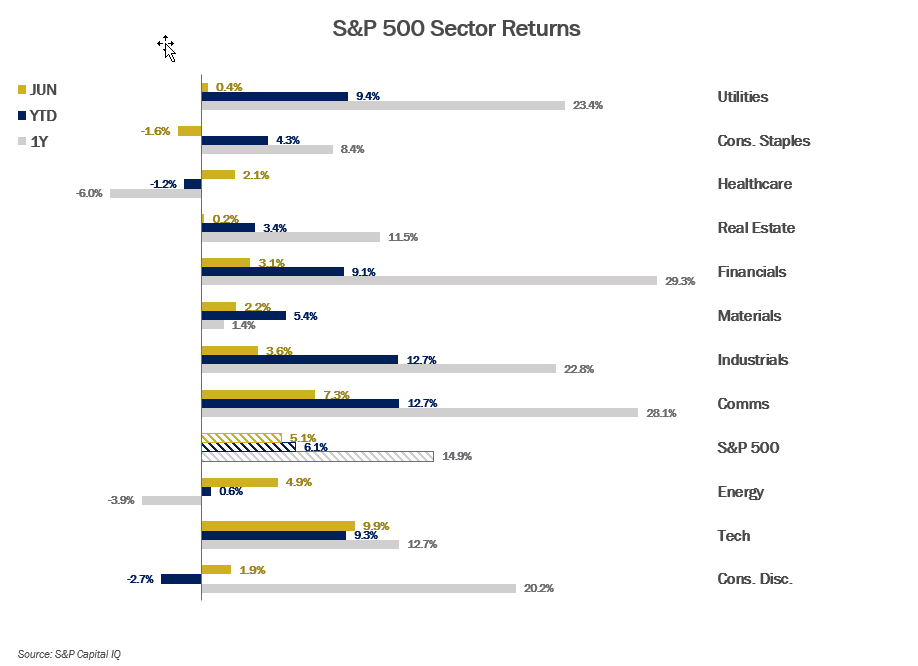

Large-cap US Stocks (S&P 500) surged 5.1% in June, capping a massive 10.9% gain for Q2 and closing out the first half of 2025 at an all-time high. Small-caps (Russell 2000) jumped 8.5% in Q2, nearly erasing their YTD losses — a sign that the rally is broad-based, not just a mega-cap story. Non-US equities (ACWI ex-US) soared 13% in Q2 and are now up 18.5% YTD, reflecting synchronized optimism across global markets. All of this occurred in a month when Israel and the US bombed Iran, and it barely registered a blip in markets outside of oil futures. The animal spirits that investors have been expecting since the election results of November 2024 finally seem to have shown up. We’re so back and as the kids would say, back from the depths of the tariff and trade uncertainty, and the vibes are immaculate. Unfortunately, we don’t actually have any certainty with respect to the ultimate policy outcome. With the passage of the OBBBA, the tax revenue aspect of tariffs no longer seems as critical in the near-term for the White House, and yet threats of very high tariffs with key trade partners has reared its head again. Markets seem to be assuming that this latest series of high tariff threats is mostly posturing and any resulting tariffs above 10% will be limited or reasonable, but as we saw in April, the policy shift only occurred once markets sold off deeply. This puts the markets in a game of chicken with the White House, and following their series of successes in June, we don’t see the White House backing down until the market swerves first.

.png?lang=en-US "07-2024-Returns.png")

Quick Hits

The Waiting Place

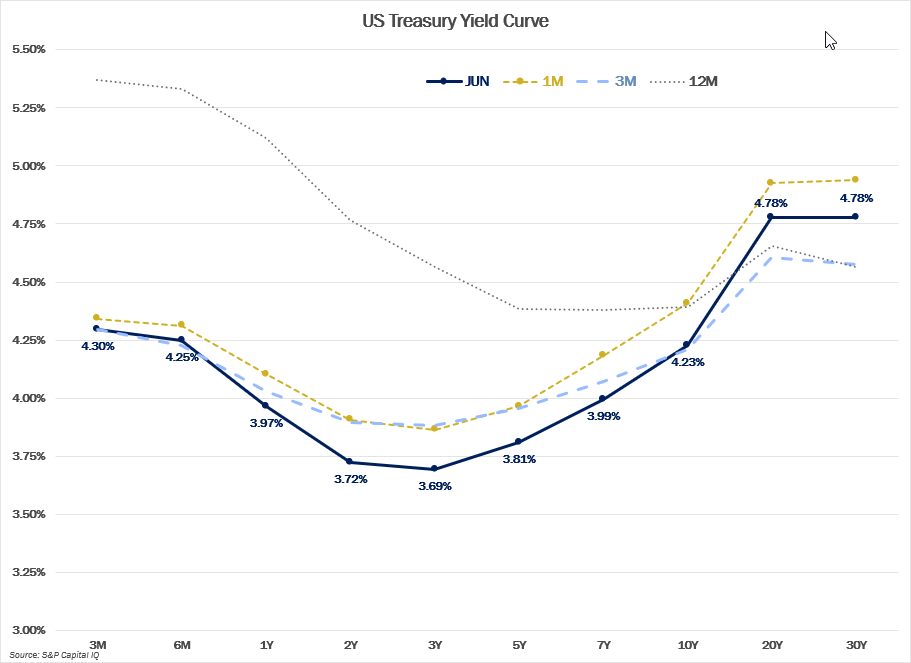

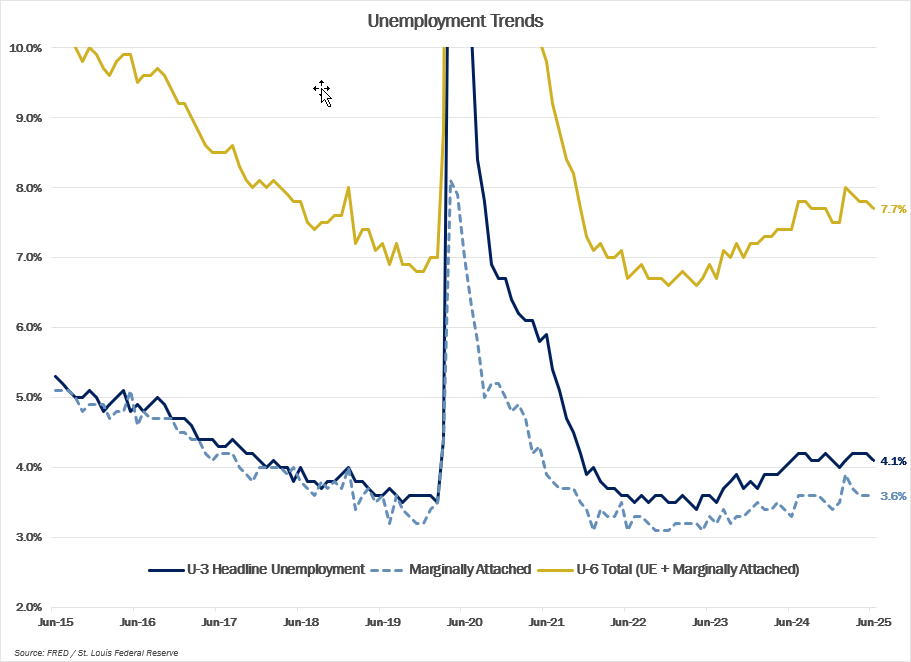

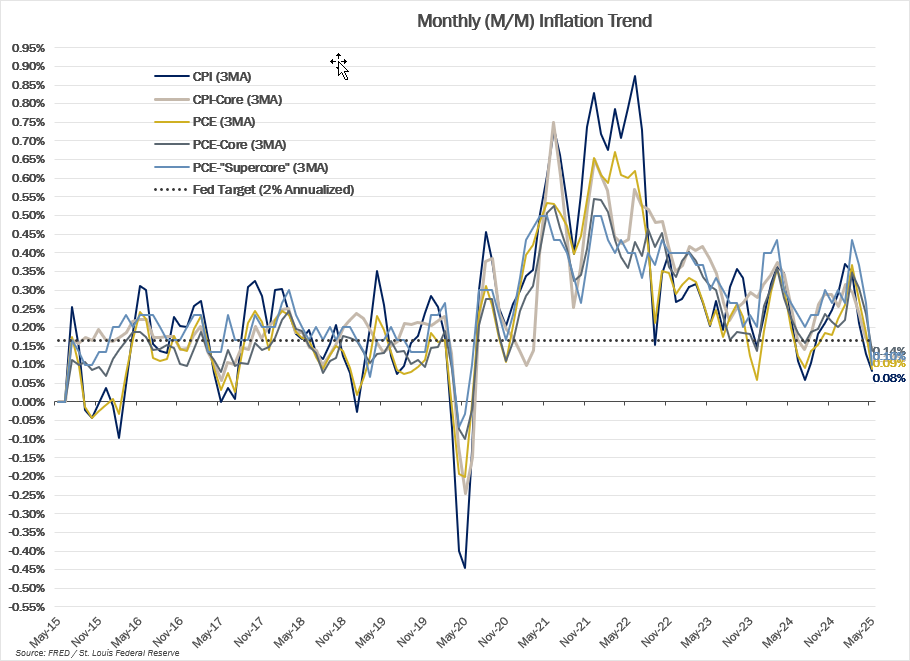

The FOMC currently finds itself in “a most useless place”, stuck waiting to see which of its mandates will set-off alarm bells first. The existing data shows that employment is fairly maximized, payroll growth remains strong and some estimates show labor force shrinking some as immigration declines. Additionally, the growth rate of inflation has made good progress towards its 2% target, but the committee continues to delay signaling rate cuts as it watches to see what impact, if any, the tariff policies have on prices in the economy. A bittersweet irony for the FOMC members, market participants, and rate-sensitive businesses is that each time tariff negotiations get punted into the future, our final “escape [from] all that waiting and staying, [where we’ll] find the bright places where the Boom Bands are playing” is subsequently delayed into the future too. For now, we and the FOMC remain in the Waiting Place.

On Deck this Month

- 07/01 – ISM Manufacturing (Jun), JOLTS (May)

- 07/03 – Employment Report (Jun), ISM Services (Jun)

- 07/04 – Independence Day Holiday

- 07/15 – CPI (Jun)

- 07/16 – PPI (Jun)

- 07/17 – Retail Sales (Jun), Import Prices (Jun), Business Inventories (Jun)

- 07/13– Consumer Price Index (Jun), NFIB Survey (Jun)

- 07/29 – FOMC Meeting, JOLTS (Jun), Consumer Confidence (Jul)

- 07/30 – Advance Estimate of 2Q 2025 Real GDP, 3rd Estimate of 1Q 2025 Real GDP

- 07/31 – PCE (Jun)

Number of the Month

Charted below are the Top 20 holdings/constituents of the S&P 500 Index as of June 2020 and more recently on July 10, 2025 when NVIDIA became the first company in history to achieve a $4 Trillion market capitalization. What we think is particularly interesting is the staggering jump in size of several of the top holdings, but also given the magnitude of the increase in market caps, how relatively little the respective index weightings shifted. This is largely due to, with the exception of NVDA, most of the top names today were already top holdings in 2020 (GOOGL, META fka FB, AMZN, etc).

Chart of the Month: Truth(s) and/or Dare

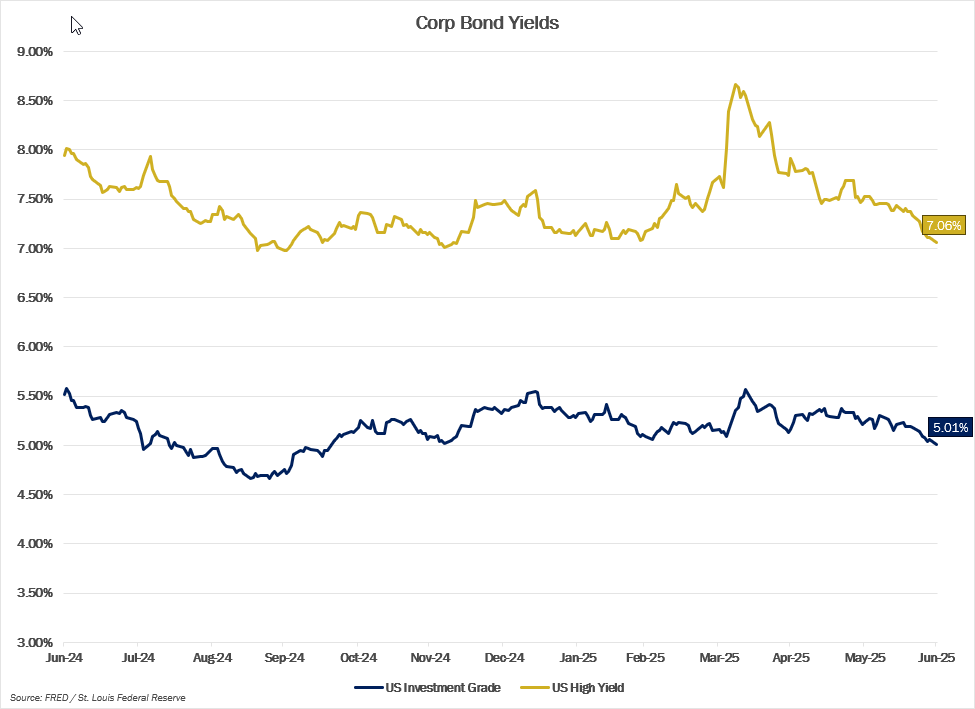

In late-June, the President, posted several times on Truth Social about his dissatisfaction with the level of interest-rates and reviving rhetoric from earlier in the year about firing the current Fed Chair or even attempting to name his successor in advance; in effect, creating a so-called “shadow Chair”. In the days immediately following the June 18 FOMC Meeting (in which the committee didn’t seem to materially shift their year-end forecast for rates), the President’s social media posts along with public commentary from some in his cabinet, and most notably, some Federal Reserve governors making public comments that many perceived as tailored for the White House, Fed Funds Futures began to price in an extra cut or two. In the absence of market moving economic data (between the June 18 FOMC meeting and the July 3 employment report), markets seemed to be pricing in the very real possibility of FOMC votes changing as members jockeyed for power in a new political reality. Once the June employment report came in strong, market pricing moved back up as there was less “economic cover” for FOMC members to shift their prior positions. This will remain a space to watch, even if Jerome Powell serves out the remainder of his term and no “shadow chair” is named, this 15-day period in markets is just the latest historical example that should remind investors that the Federal Reserve has never operated entirely in a vacuum. There are individual and institutional incentives that can have a material effect on decision-making and should not be ignored.

Equities

.png")

.png?lang=en-US "MMM-Graph-3-Equities-2.png")

Fixed Income

.png?lang=en-US "MMM-Graph-4-US-Treasury.png")

.png?lang=en-US "MMM-Graph-5-Crop-Bond.png")

Economic Data

.png?lang=en-US "MMM-Graph-6-Unemployment-Trends.png")

.png?lang=en-US "ECON-Inflation-Trend-(1).png")

Serving Generations of Texas Families

We attain an in-depth understanding of our clients’ immediate and long-term goals, collaborating with their advisors to create a comprehensive financial plan, unique to them and their family.

INVESTMENT AND WEALTH SERVICES: Not a deposit | Not FDIC insured | No Bank guarantee | May lose value