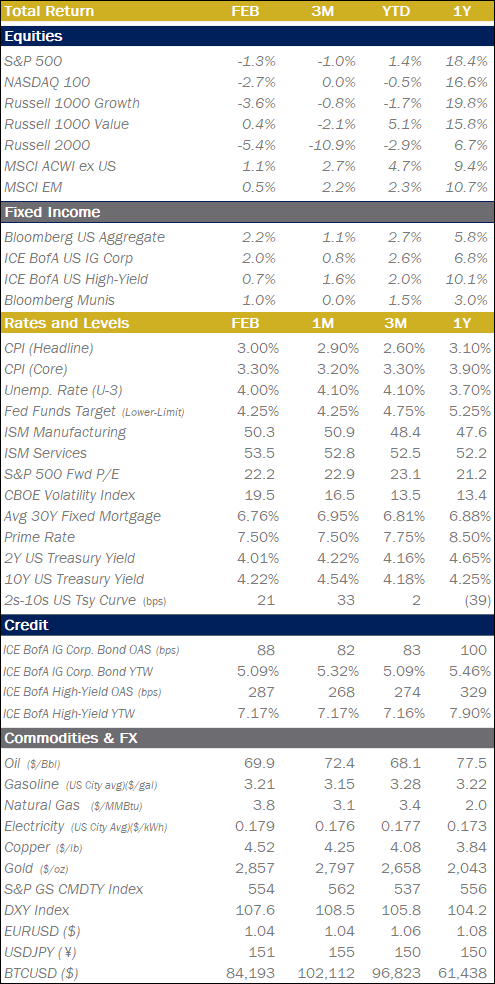

Monthly Markets Memo - March 2025

The Trump administration quickly began implementing its agenda, inspired by Silicon Valley's "Move fast and break things" ethos. The resulting uncertainty and potential disruption to government agencies could significantly impact the consumer-driven economy, requiring substantial monetary and fiscal intervention to fix.

Move Fast, Break Things

The new Trump administration didn’t waste any time getting to work implementing its agenda, which includes among many other priorities, the establishment of the Department of Government Efficiency (DOGE) under the Executive Office of the President (i.e. not cabinet-level). Led by Elon Musk and a team of data analysts and programmers, its mandate is to reduce government waste and improve its efficiency. Its methods bear a striking resemblance to the Silicon Valley ethos of “Move fast and break things,” made famous by Facebook in its early years. The goal is to prioritize growth/building/achieving results, and mistakes are a necessary part of the process that can be corrected later. While this approach certainly lends itself well to software development and high-growth startups that thrive on disruption, markets began to digest the prospect that disruption to the federal government could be further exacerbating the general uncertainty regarding the future end state of trade, labor, and tax policies. After setting new highs in the middle of the month, the S&P 500 declined sharply in the latter part of the month, ultimately ending down -1.3% for February, with bond yields declining 30-50bps across the curve from their intra-month highs. This sell-off was kicked off when consumer sentiment surveys and business surveys declined against expectations for stability or growth. Though surveys are considered soft economic data (as opposed to the “harder” economic data that federal economic agencies collect and report), it’s the first indication that markets have that the policy uncertainty is having a measurable effect on the two most important aspects of the US economy: Consumers and Services. As the administration continues its efforts to implement its policy agenda, the longer the uncertainty persists or the more unintentional damage is done to critical government agencies, the inertia of the consumer-driven economy itself could be what ultimately breaks. That is much, much harder to fix without significant monetary and fiscal intervention.

.png?lang=en-US "07-2024-Returns.png")

Quick Hits

"Buy The Rumor, Sell The News"

In the weeks after the 2024 Presidential election, the “Trump Trade” was ascendant: the prospects of lower taxes and deregulation were powering US equities higher, the prospect of tariffs and trade war was depressing Int’l stocks like the MSCI EAFE Index, and Elon Musk’s TSLA had nearly doubled by mid-December. Now as of late February, early March, the trade has come completely full circle with the S&P 500 flat to slightly negative since election day, Int’l Stocks are actually up 5%, and both TSLA and COIN (a crypto brokerage platform) have come back down to earth from being up 90% and 70%, respectively.

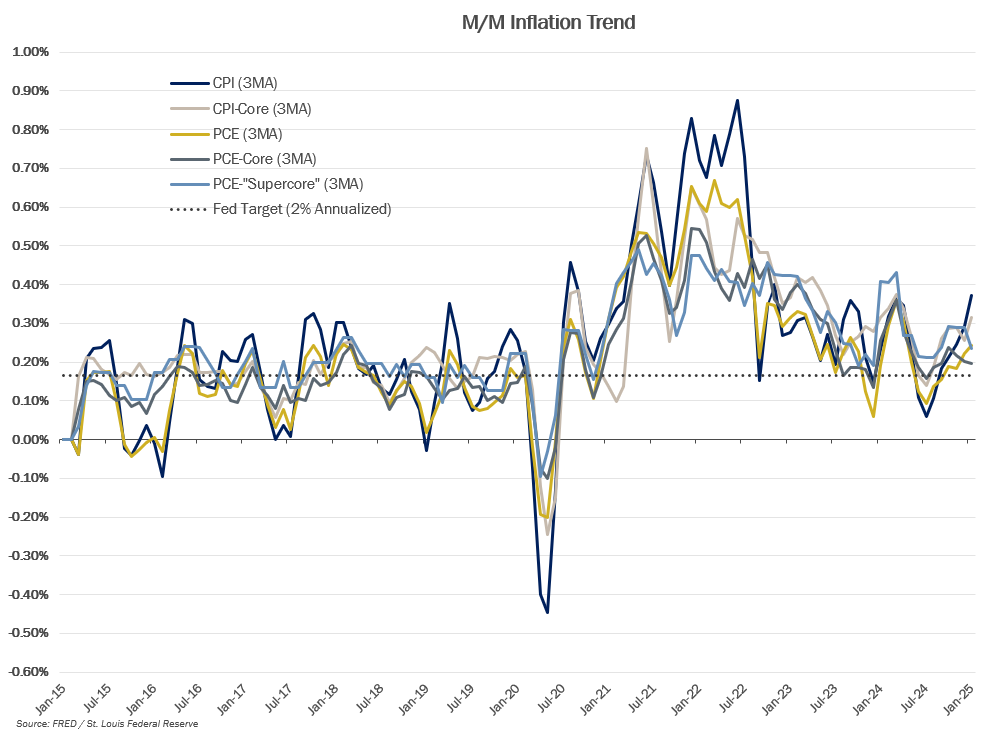

Inflation’s January Effect

January Core CPI was much hotter than expected, at 0.45% M/M and 3.0% Y/Y, this gave markets a bit of heartburn, but most economists attributed the spike to the so-called January Effect, where some calendar year price adjustments that companies implement at the beginning of each year for new fiscal years and to capture COLA adjustments drive spikes in the data during Q1. Fortunately, the FOMC uses the Personal Consumption Expenditure (PCE) measure to evaluate inflation trends in the economy. January Core PCE at 0.28% M/M and 2.5% Y/Y, much more in-line with the disinflationary trend that the Fed wants to see. PCE samples a broader range of products and services in the economy. It also adjusts the weightings of its “basket” monthly which allows for substitution effects to flow through to the data.

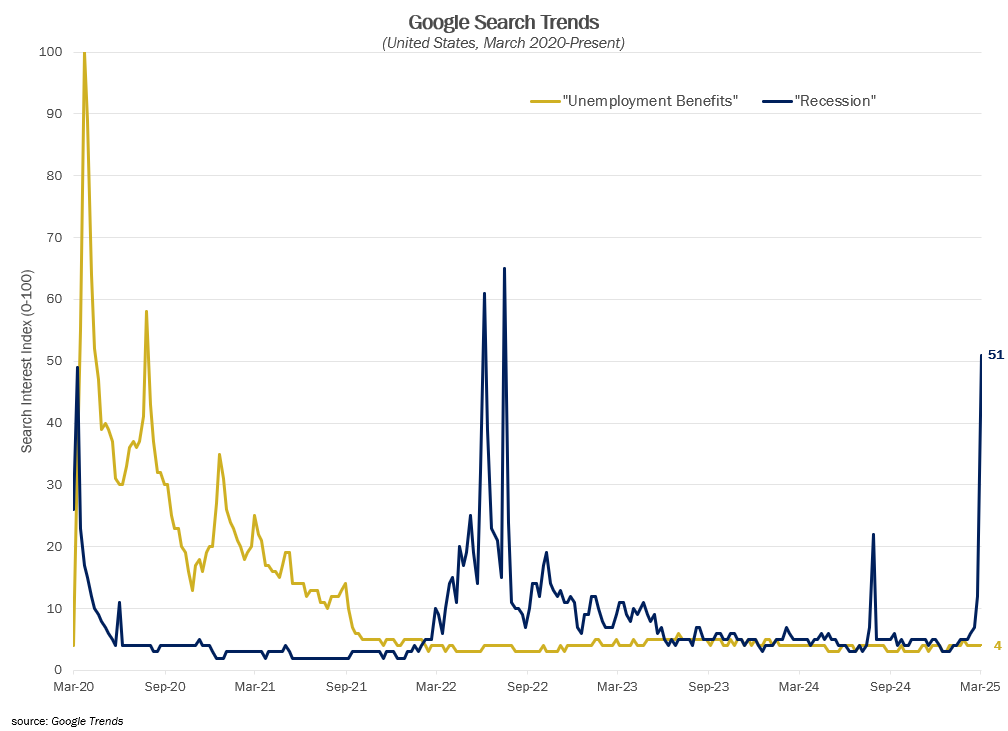

Number of the Month

Any time there is significant market volatility and negative economic news, Google searches for “Recession” will spike. A key “canary in the coal mine,” using the same Google Trends that could indicate if general anxiety about the possibility of recession is converting into an actual recession would be a spike in users inquiring about “Unemployment Benefits,” as a proxy for layoffs or increasing unemployment. Fortunately, while the popularity index of “Recession” has spiked significantly with the recent correction in US equities, we are not yet seeing any sign of increasing searches for “UE Benefits.”

.png?lang=en-US "Number-of-the-Month-(Google-Trends).png")

On Deck this Month

- 03/03 – ISM Manufacturing (Feb)

- 03/05 – ISM Services (Feb)

- 03/07 – Employment Report (Feb)

- 03/11 – Job Openings & Labor Turnover Survey (JOLTS) - Jan

- 03/12 – Consumer Price Index (Feb)

- 03/13 – Producer Price Index (Feb)

- 03/17 – Retail Sales (Feb)

- 03/19 – FOMC Meeting (with Summary of Econ Projections)

- 03/20 – Existing Home Sales (Feb) & start of NCAA Men’s Basketball Tournament

- 03/24 – Manufacturing and Services PMIs (Mar Flash)

- 03/27 – 3rd Estimate Real GDP (Q4)

- 03/28 – PCE (Feb)

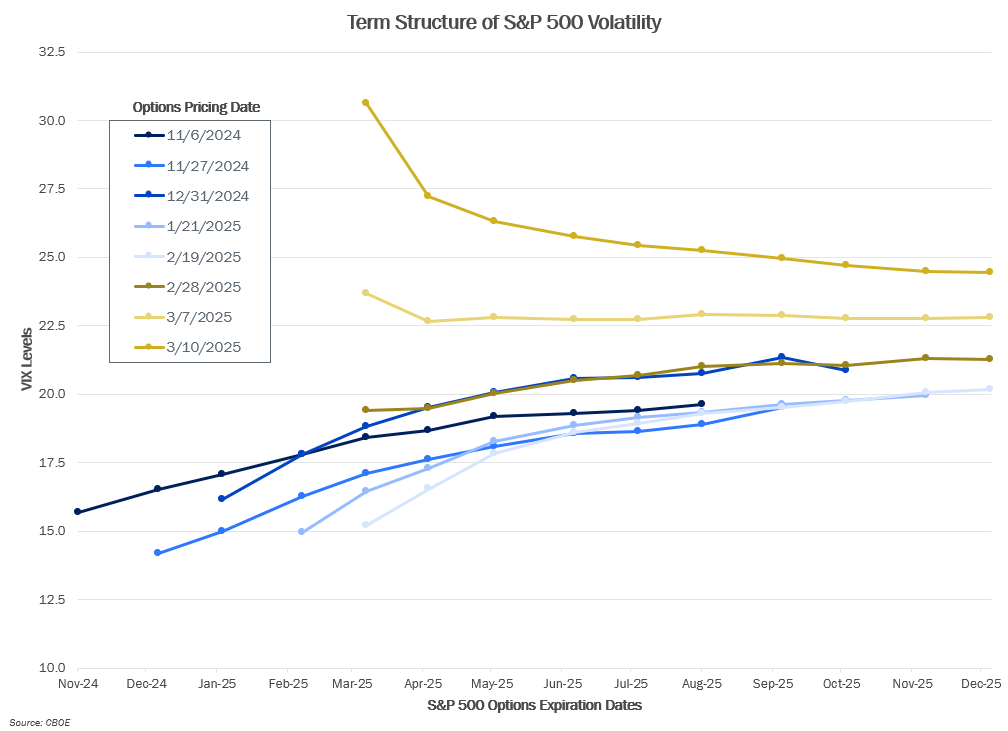

Chart of the Month: Cranking up the Vol

The term-structure of volatility expectations has shifted up significantly in the month of February and first part of March. Typically, near-term volatility is priced low and prices higher the further out into the future you go. During periods of high volatility or uncertainty, the front end of the curve will be high and will slope back to “normal” levels as markets expect the source of volatility to be resolved over time. What we’re seeing currently is a relatively flat curve that tells us markets don’t really know when to expect resolution on the current sources of uncertainty in the markets.

.png?lang=en-US "MMM-Graph-2-Credit-Spreads.png")

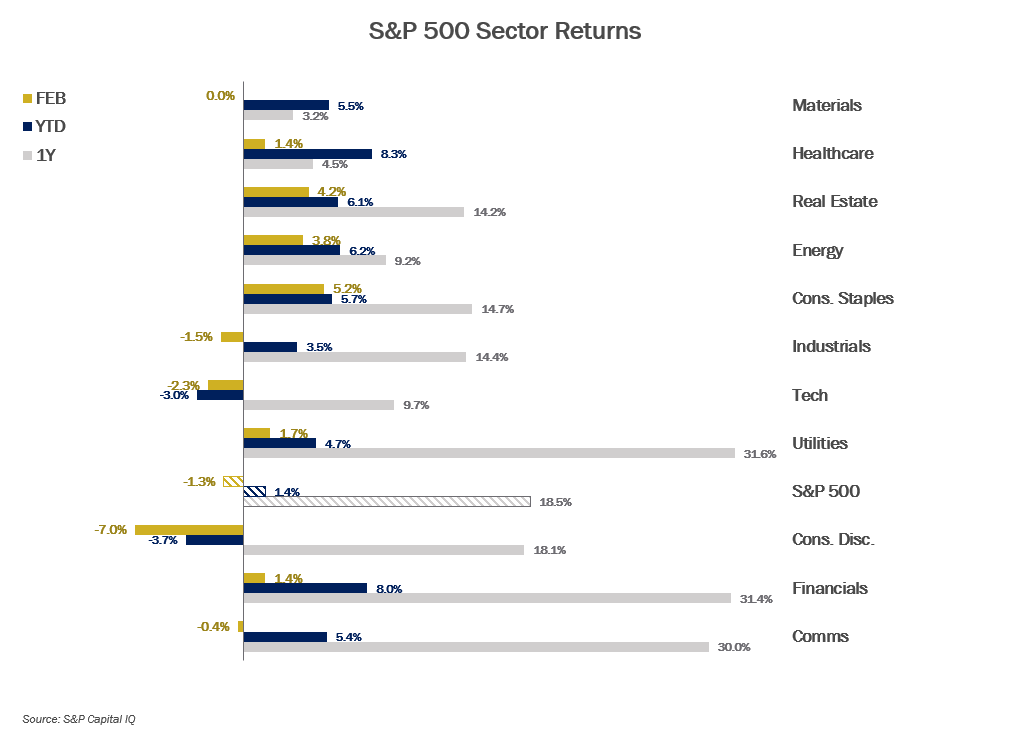

Equities

.png")

.png?lang=en-US "MMM-Graph-3-Equities-2.png")

Fixed Income

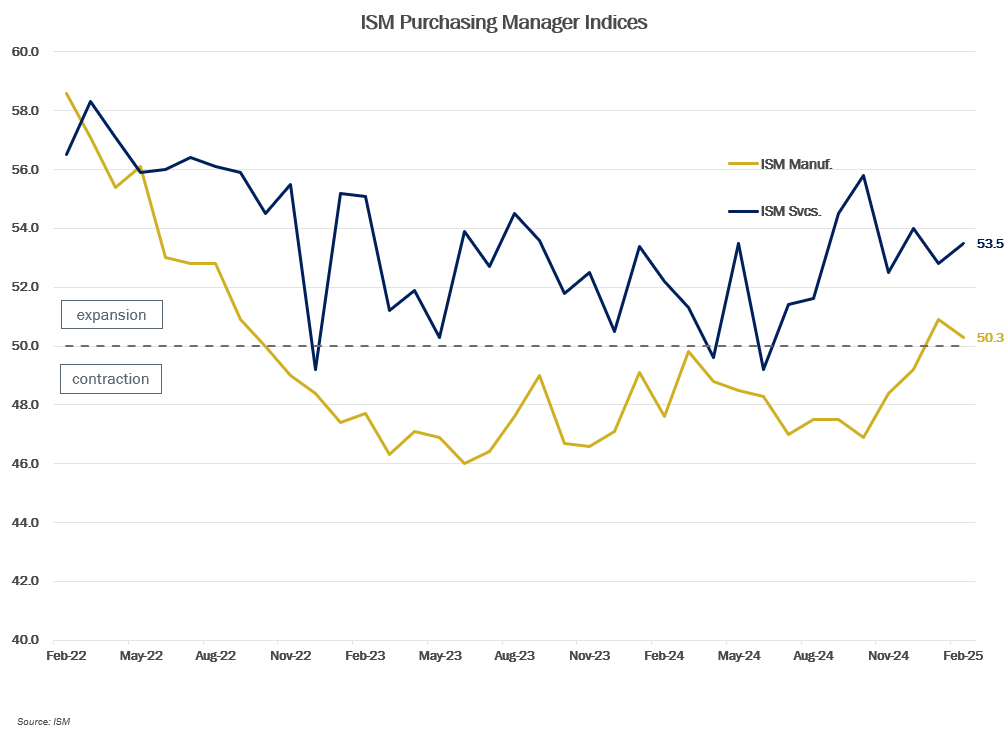

Economic Data

.png?lang=en-US "MMM-Graph-7-ISM.png")

.png "ECON-Inflation-Trend-(1).png")

Serving Generations of Texas Families

We attain an in-depth understanding of our clients’ immediate and long-term goals, collaborating with their advisors to create a comprehensive financial plan, unique to them and their family.

INVESTMENT AND WEALTH SERVICES: Not a deposit | Not FDIC insured | No Bank guarantee | May lose value