Monthly Markets Memo - November 2024

October brought a mix of optimism and caution as the markets respond to the latest economic signals. The Federal Reserve's recent decisions continue to shape the financial landscape, with investors closely watching for any shifts in policy. As the year draws to a close, staying informed and adaptable remains crucial for navigating the complexities of the market.

October Surprise

October is often associated with falling temperatures, leaves changing colors, and pumpkin spice somehow finding its way into just about every food or beverage for sale. The FOMC cut rates by 50bps to 4.75-5.00% on September 18th, and this was intended to signal that the committee was very much focused on reducing its restrictive monetary posture and that it was not “behind the curve” on reacting to weakness in the labor market. Welp, twelve days later the September employment report showed growth in payrolls way above expectations at 223k jobs and the unemployment rate fell a tenth of a point to 4.1%. This reduced the pressure and urgency on the Fed to cut and soon the market was pricing fewer cuts and further out into the future, and the immediate effect was rising yields across the curve, increasing by nearly 50bps (as much as the Fed had just cut the funds rate) in some tenors, like the 2Y Treasury. This likely came as a very unwelcome and disappointing surprise to many business owners and homebuyers who have been waiting for “the Fed to lower interest rates” so they can expand their businesses or buy homes at affordable rates. It’s like U.S. borrowers went trick-or-treating expecting full size candy bars, and instead got tricked with dental floss and toothbrushes. (apologies to the dentists in our audience).

Number of the Month

The jaw-dropping amount of money spent purchasing airtime for political ads on broadcast TV this year. I don’t think we’ve ever been so excited to be see TV ads for insurance, fast food, and cars grace our screens once again.

Quick Hits

Simmering Geopolitical Beef

Israel and Iran almost graduated from local proxy war to direct regional war as they traded cruise missiles, drones, and airstrikes originating from their own soil. Fortunately, for the region and the world, the cycle of escalation subsided for now. It was another example of potential exogenous shocks to the global economy that can arise suddenly from long-simmering hot spots (e.g. Ukraine, Middle-East, etc.) but that markets have grown accustomed to ignoring.

Earning it

Q3 earnings season kicked-off in October and results are impressive so far, with most S&P 500 companies beating consensus estimates on both revenue and earnings. Full-year 2024 estimated earnings for S&P 500 companies are set to increase 15% vs. 2023, and 2025 estimates reflect 10% growth. It shouldn’t be any surprise to note that once you bifurcate the S&P 500 between the “Magnificent 7” and the other 493 companies, the Y/Y earnings growth in Q3 is 23.4% vs. 2.6%, respectively. This isn’t the dot-com bubble 2.0, where it was all multiple-expansion built on hopes and dreams. These companies have achieved mega-capitalization levels and some of the highest Fwd P/E valuations we’ve seen since the dot-com bubble era because of the incredibly strong earnings growth they’re displaying. It’s a virtuous cycle that continues to defy gravity.

Floored

Inflation, though trending downwards, is still not where the FOMC has stated they would like it to be. Thanks to significant declines in energy cost over the past year, the headline measures of CPI and PCE are showing growth in the 2.0-2.5% range, but once you strip out the volatile food & energy components, you’ll see that inflation has hit a floor around 3% in the past few months with very little downward movement in the Shelter component which is one of the largest components of both inflation indices, and the more acute measure of people’s wallets. The Shelter component is inflating at a 4-5% annual rate consistently over the past year. Until we see significant downward movement in shelter costs, we likely won’t see any of the core measures of inflation reach the Fed’s target.

On Deck this Month

- 11/01 – Emp. Report (Oct) & ISM Manuf. (Oct)

- 11/05 – ISM Svcs. (Oct)

- 11/05 – Election Day

- 11/07 – FOMC Meeting: Rate Decision and Press Conf.

- 11/11 – Veterans Day (Banks and Bond Market Closed)

- 11/13 – Consumer Price Index (Oct)

- 11/14 – Texas HS Football Playoffs begin

- 11/15 – Retail Sales (Oct)

- 11/27 – Q3 Real GDP (2nd Estimate) & PCE (Oct)

- 11/28 – Thanksgiving Day (Markets Closed)

- 11/30 – Texas A&M vs. Texas (First football game since 2011)

Chart of the Month: Outrageous Demand

Continuing with last month’s spotlight on Utilities and Independent Power Producers, ERCOT updated its annual Long-Term Load Forecast this past summer and it’s striking how the estimates for peak demand have skyrocketed in just a single year as market participants begin to grasp the intensity of power demands from AI-focused datacenters and the massive impact of new industrial infrastructure (Hydrogen, Battery, EV, LNG, etc.) scheduled to come online across the state in the next few years. To put it in stark relief, the prior forecast showed peak demand growth estimated to grow at a plodding but respectable 1.4% annually from 2024 through 2028. Now the grid operator is expecting **12.4%** annual growth over the same period. The 2028 peak load estimate for 2028 was ramped higher from 89 GW to 137GW, that’s a nearly 50GW jump. For context, 55GW is the EIA estimate for all new installed generation capacity across the entire U.S. for 2024. This should serve as yet another reminder that while the long-term cash flows/returns/productivity gains from AI might be squishy and highly uncertain, there are billions of real dollars being invested in hard assets and infrastructure today that will have real economic impact across the state, the country, and the world.

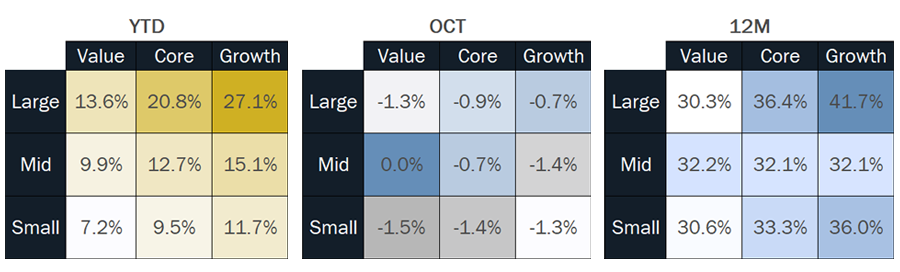

Equities

.png?lang=en-US "MMM-Graph-3-Equities-(2).png")

Fixed Income

Economic Data

Serving Generations of Texas Families

We attain an in-depth understanding of our clients’ immediate and long-term goals, collaborating with their advisors to create a comprehensive financial plan, unique to them and their family.

INVESTMENT AND WEALTH SERVICES: Not a deposit | Not FDIC insured | No Bank guarantee | May lose value