Monthly Markets Memo - October 2024

September data continues to be choppy, with lots of noise and head fakes, just as it was over the past year that saw the FOMC “talking about” rate cuts to finally, actually cutting.

The First Cut is the Deepest

Chair Powell and the FOMC embarked on the first (non-pandemic) easing cycle since August of 2019 with a hefty 50bps cut of the Federal Funds Target range to 4.75-5.00%. Further, they signaled a front-loaded path to “normalization” via the quarterly Summary of Economic Projections (a.k.a. Dot plots), which showed their median estimate of the Fed Funds Rate for December 2024 and December 2025 at 4.25-4.5% and 3.25-3.50%, respectively. That’s 100bps of cuts this fall, and an additional 100bps through next year, with most of those cuts expected to occur in the first half of 2025. If a chonky 50bps cut from the FOMC wasn’t strong enough evidence of a “recalibration” of the FOMC’s views regarding risks to the economy from a slowing labor market, the speech and Q&A from Chair Powell at the National Association of Business Economists (NABE) conference at the end of September should have done the trick. Powell, as always, emphasized data dependency, but that data he referenced was very much focused on jobs. He particularly cited slowing payroll growth that was concerning to the committee: “the level of job creation is maybe not quite at the level it needs to be to hold unemployment constant given assumptions about supply.” As we progress through the next few months, the FOMC and markets will be very focused on labor market data, such as weekly Initial UI Claims, monthly Employment Report, monthly Job Openings and Labor Turnover Survey (JOLTS). Any indication of further slowing in hiring or any sign of layoffs will likely accelerate the expected rate cutting pace of the FOMC. The opposite will hold as well: any signs of unexpected labor market strength could likely slow the pace of interest rate normalization or the anticipated terminal level for the federal funds rate. We anticipate data will continue to be choppy, with lots of noise and head fakes in the data, just as it was over the past year that saw the FOMC “talking about” rate cuts to finally, actually cutting.

.png?lang=en-US "07-2024-Returns.png")

Number of the Month

Days since the S&P 500 bottomed on October 12, 2022 amidst fears of runaway inflation and the Fed’s rapid increase of rates to combat it. It's doubtful anyone would describe the last 719 days as easy breezy, smooth sailing in markets or geopolitics, and yet, the bull market has marched onward. Through September month-end, the S&P 500 has returned 69% since the October 2022 low, has set several new all-time highs and has returned roughly 30% from the previous high set in December of 2021. Most interesting and unexpected, this has occurred during an inverted yield-curve.

Quick Hits

It’s Debatable

The nation got its first and likely only debate between Vice President Kamala Harris and former president Donald Trump, and while in the week afterwards it seemed there was an impact that saw some movement towards Harris in the polling averages, that phenomenon has since faded and reversed. Polling averages in the key electoral states (AZ, GA, MI, NV, NC, PA, & WI) have the two candidates trending within 1pt or less of each other and are well within margins of error. Given the tightness of the race, the inevitable recounts, lawsuits, etc., it’s very possible that by the time the next Monthly Markets Memo publishes, we still might not know who our next President will be.

China Trying to Light Fuse

The People’s Bank of China (PBOC) announced a monetary stimulus package intended to jolt a slowing economy. China’s economic malaise, and its government’s perceived apathy towards it has surprised investors and observers for the past couple of years. It was anticipated that with government’s ending of its draconian zero-COVID policy of mass lockdowns, that the Chinese economy would be coiled and ready to spring upwards. This resurgence never materialized as consumption and investment declined, as a result of global inflation and the fallout from the ongoing real estate crash in China. These new measures from the Chinese central bank, and the fiscal measures that will hopefully be announced in coming weeks or months, will hopefully allow the Chinese economy to pivot in a positive direction. While China as a nation state is a clear rival to the US, it remains a critical market for US services and products, and an integral part of the supply chain. In other words, the US economy largely does well when the Chinese economy is doing well.

“The Two Utes”

Raise your hand if you had Utilities as the best performing sector in the S&P 500 for 2024 on your bingo card. If your hand is raised, you’re either a genius or a liar. While utilities often do well in a falling-rate environment, as their underlying margins are often locked in at the prior rate levels and flow through to large dividends relative to the rest of the index, that alone is not what is driving this outperformance. It’s the Independent Power Producers (IPPs) within the sector that are driving this outperformance, and it’s entirely driven by the market’s search for the next layer of winners to benefit from the AI revolution. As we highlighted in last month’s memo, there are tens of billions being spent on capital to build datacenters to drive the training of these nascent AI models. But once you’ve purchased the land, engaged the contractors, and ordered the chips, what else is needed? Power. So, so many Gigawatts of dedicated power, and this is where you’re seeing some big IPP names like Constellation Energy (CEG) and Vistra Corp. (VST) benefit from this next phase of the AI halo extending out through equities. Both CEG and VST are up 123% and 210%, respectively in 2024. To illustrate the scope and urgency of need to secure power for the so-called hyperscalers, Constellation recently announced that thanks to a long-term supply contract with Microsoft, it would be restarting the long-dormant, remaining reactor at the infamous Three Mile Island power station.

On Deck this Month

- 10/01 – ISM Manuf. (Sep)

- 10/03 – ISM Svcs. (Sep)

- 10/04 – Emp. Report (Sep)

- 10/10 – Consumer Price Index (Sep)

- 10/11 – CPI (Sep) & Large Banks kick-off Q3 earnings season

- 10/14 – Columbus Day (Bank & Bond Market Holiday)

- 10/21 – Early Voting Begins in Texas

- 10/29 – JOLTS (Aug)

- 10/30 – 3Q Real GDP (1st Estimate)

- 10/31 – PCE (Sep) & Emp. Cost Index (Q3)

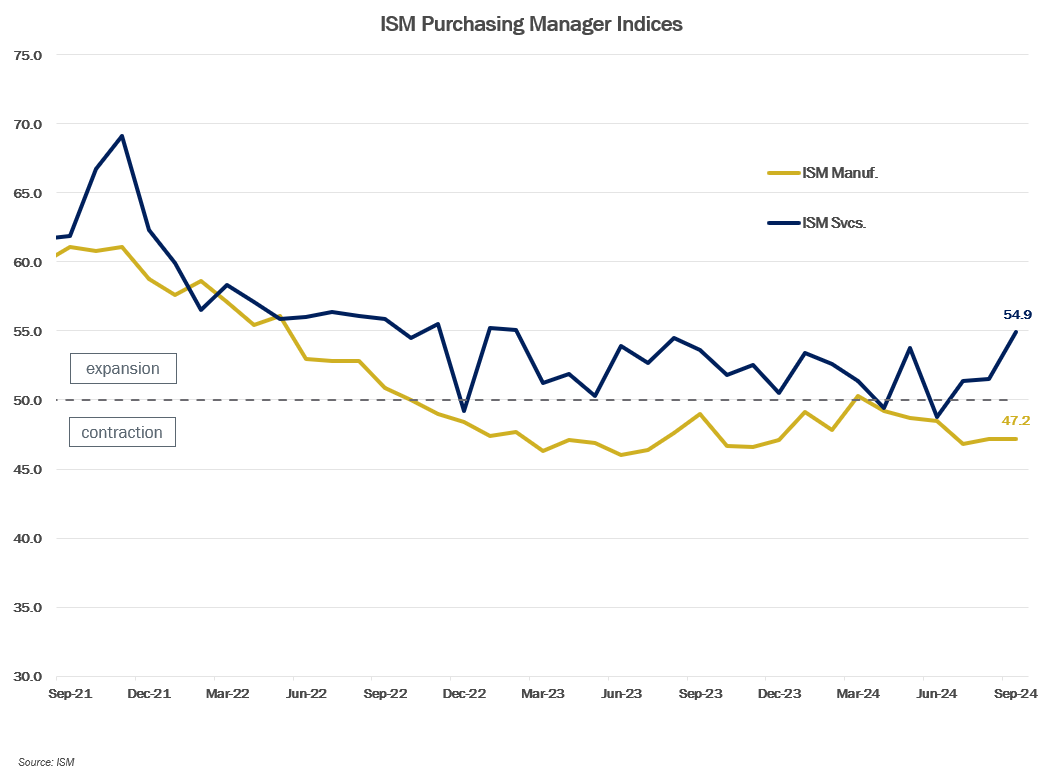

Chart of the Month: Because I was Inverted

793 Days. This was the longest US Treasury yield curve inversion (as measured by the spread between the 2Y Yield and 10Y Yield) ever recorded. From July 5, 2022 to September 5, 2024, the short end of the curve was higher than the longer end, defying the “normal” shape of the curve and the usual term structure of interest rates (i.e., the longer the term, the more compensation should receive for the increased risk). Yield Curve inversions are often framed as a recession forecast by the bond market. While this is often true (roughly 80% of yield curve inversions have been followed by recessions), it is undeniably true that they are indicative of actual or anticipated monetary policy conditions that disincentivize longer-term investment and risk-taking in the economy. When the short-end of the curve is higher than the long-end (e.g., when the FOMC aggressively raises the federal funds rate), rational investors will keep their money parked in relatively safe short-term investments since that is where risk-adjusted returns are maximized in an inverted yield curve environment. As we move from inversion to flat to a normalized, positively sloped yield curve, we will be eager to see in which parts of the economy this developing tailwind manifests itself first.

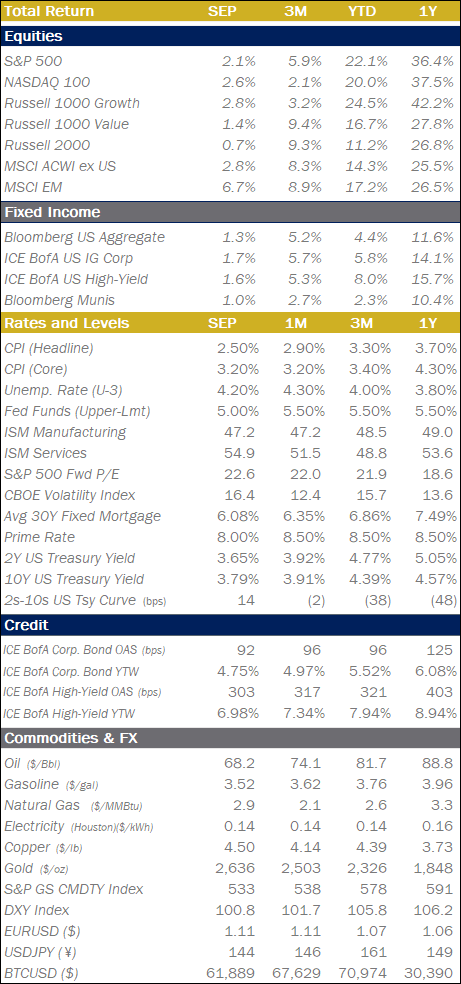

Equities

.png")

Fixed Income

Economic Data

.png?lang=en-US "MMM-Graph-7-ISM.png")

Serving Generations of Texas Families

We attain an in-depth understanding of our clients’ immediate and long-term goals, collaborating with their advisors to create a comprehensive financial plan, unique to them and their family.

INVESTMENT AND WEALTH SERVICES: Not a deposit | Not FDIC insured | No Bank guarantee | May lose value

*Toy Story (1995). Directed by John Lasseter, Buena Vista Pictures Distribution, 22 Nov. 1995.